China has set a goal of 5% GDP growth, 3% consumer price inflation, and an unemployment rate of 5.5% in 2023. The government is prioritizing domestic demand and expanding consumption. In 2M23, exports in USD terms fell 6.8%, more than expected, while imports dropped 10.2%, worse than expected, indicating that domestic demand may still be weak. However, with policy support, the recovery of domestic demand-related sectors is expected to accelerate and outperform the market. According to market data, sales for global semiconductor industry in January 2023 were $41.3 bn, -5.2% MoM and -18.5% YoY. The industry is still in a downward cycle, and there is still downward pressure on the semiconductor-related industries.

The Hong Kong stock market has been more volatile recently, the VHSI (Volatility Index) of the Hang Seng Index has shown a significant increase (to ~27), reflecting the increase in market’s risk aversion. The Hang Seng index dropped below the 20,000 points level, also below the 10 days, 20 days, and 250 days SMA, indicating a weakening technical trend. China has set a more conservative growth target of 5% this year, which is 0.5 percentage points lower than last year’s target, there may not be too many positive stimulus measures to support the investment market. The probability of a 0.5% rate hike in US rate in March has risen from about 22% to nearly 40%, and the inverted yield-spread between 2-year and 30-year US bond yields has touched a record high (108.96 basis points). With concerns about accelerated rate hikes and recession risks, we expect Hang Seng Index to remain weak and trade between 18,500 and 20,500 points.

Energy and Telecommunications outperformed the markets. However, we expect limited upside from here without more catalysts. Benefiting from policy support, we expect consumer-related companies to outperform the market.

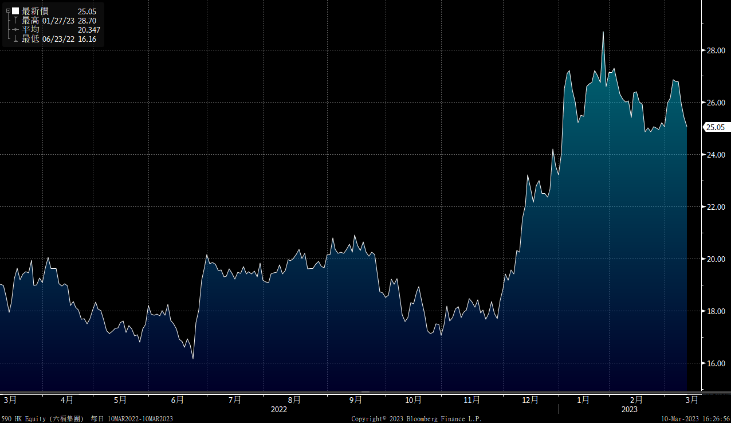

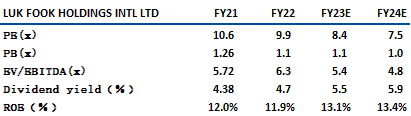

Luk Fook (590) is principally engaged in the sourcing, designing, wholesaling, trademark licensing and retailing of a variety of gold and platinum and gem-set jewellery. In 4Q22, the company’s overall SSSG turned from positive to -10%, mainly due to the rebound in gold prices and resurgence of Covid in China. The SSSG for gold products/ gem-set jewellery during 4Q22 were -5% and -21% respectively. By region, SSSG for Hong Kong and Macau markets was -8%, and China was -35%.

Benefited from Hong Kong China border reopening, the company’s sales had rebounded significantly. Sales in Hong Kong have returned to pre-Covid levels. Mgmt targets double-digit YoY growth in sales for 23E and single-digit YoY growth in net profit. In terms of expansion plans, net store openings for 23E dropped from 500 to 300 but the target for 24E was maintained at 500. Since the company’s current rental expenses is only at ~50% compare to pre Covid level, whilst China tourists accounts for nearly 60% of sales in HK pre-Covid, we expect company’s sales to further improve. It is recommended to buy at $24.0, target at $27.0, stop loss at $22.5. Risks: Retail sales recovered slower than expected.

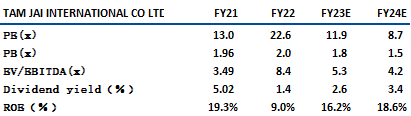

Tam Jai International (2217) is a leading and renowned restaurant chain, operating the TamJai (譚仔雲南米線) and SamGor (譚仔三哥米線) branded fast casual restaurants in Hong Kong. Currently, it has 208 restaurants around the world. In FY1H23, the company’s revenue fell 6.8% YoY to HK$1.26 bn, and net profit fell 40% YoY to HK$82.77 mn, mainly due to a 13.1% YoY increase in costs of F&B to HK$302 million, and the staff costs increased 13% YoY to HK$405mn.

Benefiting from Hong Kong China border reopening and the distribution of HK$5,000 electronic consumer vouchers, it is expected to have a positive impact on the company’s revenue. Hong Kong continues to be the company’s focus, management target to increase the number of restaurants in Hong Kong from 180 to 220-250, an increase of 22%-40%. In the long run, the company also hopes to expand overseas to diversify its revenue source. The company aims to increase the contribution from overseas from the current 5% to 20% by FY27. We believe the company’s operating performance to have bottomed and recommend to buy at 2.2, target at $2.5, stop loss at $2.08. Risks: Overseas expansion plans are slower than expected.

HSI:

Source:Bloomberg

Key events for the week:

CATHAY PAC AIR (00293.HK): 2022 loss deepens to HK$6.55 bn |

CPI for February in China rose by 1% YoY, lower than the expected 1.9% and January’s 2.1%, and fell by 0.5% MoM |

PPI for February in China -1.4% YoY, lower than the expected -1.3% and January’s 0.8%, stay flat MoM |

AIA (01299.HK): NP dropped 96% YoY to US$282mn, worse than expected |

MTR CORPORATION (66.HK): NP increased 2.9% YoY to HK$9.8bn |

| Key events for next week: | |

|---|---|

|

03/15 |

Fixed asset investment, retail sales, industrial added value, Ping An (2318) results, CK Infrastructure (1038) results |

Sector performance:

| 1week performance(%) | |

|---|---|

|

Utilities |

-3.8% |

|

Real estate |

-6.5% |

|

Industrial |

-6.3% |

|

IT industry |

-9.6% |

|

Financial |

-4.5% |

|

Energy |

-0.5% |

|

Raw material |

-6.1% |

|

Medical and health care |

-8.5% |

|

Telecommunications |

-0.4% |

|

Consumer discretionary |

-7.8% |

|

Consumer staples |

-4.1% |

Source:Bloomberg

Stock pick: China Railway Luk Fook (590)

Stock pick: Tam Jai International (2217)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓