China has released several economic data, the retail sales during 2M23 increased by 3.5% YoY to CNY 7.7 tn, in line with expectations. Meanwhile, real estate development investment during 2M23 fell by 5.7% YoY to CNY 1.37 tn but still better than the expected -8.5% YoY. In terms of the labor market, the urban unemployment rate was 5.6% during 2M23, higher than the expected 5.3%, and +0.1% MoM. Although overall data reflects that China’s economy continues to recover, under increasing uncertainties in the EU and US, growth momentum of China’s economy still faces downward pressure. We expect the short-term focus of the investment market to be the liquidity issues in the US banking sector and financial system risks. Hong Kong stocks market is expected to be more volatile.

The Hong Kong stock market remains volatile, the VHSI (Volatility Index) of the Hang Seng Index increased to above 30 at one time, reflecting the increase in market risk aversion. The Hang Seng index has yet to return to the 20,000 points level and remains below 10-days, 20-days, and 250-days SMA, indicating a weak technical trend. The market is currently focused on the interest rate hike in March and liquidity issues in the US banking industry. Although the probability of a 0.25% interest rate hike in March has increased to ~60%, and the market expects no interest rate hike in May. However, we expect investors to be worried about whether the recent liquidity and confidence crisis in the US banking industry will affect other industries, including startups and technology companies. Investment sentiment is difficult to improve in the short term. In addition, China’s inflation data was lower than expected, the recovery of domestic demand may also be a concern. We expect the upside of the Hang Seng Index to be limited and trade between 19,000-20,000 points.

Utilities, telecommunications, and healthcare outperformed the market, which may reflect investors’ preference for defensive stocks under current market conditions. In addition, due to the recovery of the property market, we expect that SOEs developers and building materials have the potential for revaluation.

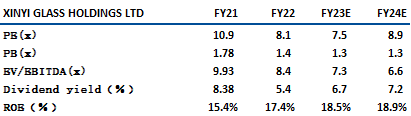

Xinyi Glass (868) is principally engaged in the production and sales of float glass, automotive glass, and architectural glass products. In 2022, the company’s revenue was HK$25.74 bn -15.5% YoY. Among them, float glass, which was accounting for 64% of revenue, decreased by 24% YoY to HK$16.58 bn, mainly due to the weak sentiment in the property market and reduced demand. Revenue from auto glass, which was accounting for 24% of revenue, was HK$6.08 bn, up 11.4% YoY. The profit for the period was HK$5.127 bn, -55.6% YoY.

Benefiting from more supportive policies for the property market, we believe that the demand for float glass will gradually recover. Coupled with the low base in 2022, we expect the company’s performance to improve. In addition, the ASP of float glass has rebounded while the major costs (soda ash and natural gas) are also expected to stabilize. We expect the profit per ton to improve. In addition, the company also plans to expand its auto glass production capacity by 5.3% in 23E, which is expected to further drive the performance. If the property market sentiment continues to improve, we expect the company’s float glass business to rebound materially. It is recommended to buy at $13.5, target at $15.2, stop loss at $12.7. Risk: The inventory of float glass is still high, which may limit the upside for ASP.

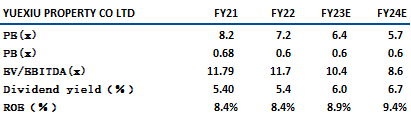

Yuexiu property (123 HK) engages in development, selling, management and holding of investment properties. The contracted sales in 2022 was CNY 125bn, +8.6% YoY, outperforming peers’ drop of ~40% YoY. Sales likely to remain solid in 23; the contracted sales for 2M23 was CNY 22.4bn, +185% YoY, while peers had dropped ~5%.

Yuexiu property (YP) has a SOE background with a healthy financial position, the average cost of borrowing was ~4%, lower than peers ave of ~6%. The company’s land reserves are mainly located in first- and second-tier cities, accounting for nearly 93% of the land bank. We believe sales to be more promising with TOD projects (“rail +property” development model) the differentiator. The projects are mainly located in prime areas with higher margin (GPM 25%-30% vs 15%-20% from land auctions). Yuexiu had extended its TOD projects to Hangzhou Metro during 22 and hope to further expand to other regions. GFA of TOD projects amounted to 3.86m s.qm, accounting for ~13.6% of total GFA. Mgmt hope to add 1-2 TOD projects each year with sales contribution of ~20%. We expect the company’s sales performance to continue to outperform its peers. It is recommended to buy at HK$11.50, target at HK$13.0, and stop loss at HK$10.8. Risks: Mgmt expects operating cash flow in 23E to be lower than 22.

HSI:

Source:Bloomberg

Key events for the week:

HKELECTRIC-SS (02638.HK):2022 NP was $2.95bn, + 0.7% YoY |

Electricity generated in China during 2M23 +0.7% YoY |

Real estate development investment for 2M23 fell by 5.7% YoY to CNY 1.37 tn |

Retail sales during 2M23 increased by 3.5% YoY to CNY 7.7 tn YoY |

Urban unemployment rate was 5.6% in 2M23 |

| Key events for next week: | |

|---|---|

|

03/20 |

Sunny Optical (2382 HK) Results |

|

03/21 |

Anta (2020 HK) Results, Geely (175 HK) Results, Henderson Land (12 HK) Results |

Sector performance:

| 1week performance(%) | |

|---|---|

|

Utilities |

2.1% |

|

Real estate |

2.6% |

|

Industrial |

1.3% |

|

IT industry |

2.6% |

|

Financial |

-0.1% |

|

Energy |

2.8% |

|

Raw material |

-0.1% |

|

Medical and health care |

2.7% |

|

Telecommunications |

5.0% |

|

Consumer discretionary |

1.2% |

|

Consumer staples |

2.5% |

Source:Bloomberg

Stock pick: Xinyi Glass (868)

Stock pick: Yuexiu property (123 HK)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓