China’s official manufacturing purchasing managers’ index (PMI) in February was 52.6, the highest since April 2012, also higher than the expected of 50.6 and 50.1 in January. The non-manufacturing PMI in February was 56.3, higher than the expected of 54.9 and 54.4 in January. The data reflect that the recovery momentum of the economy has strengthened, which has also driven the investment sentiment for HK and China market. The property sales in Feb were CNY 461.5 bn, +14.9% YoY /+29.1% MoM, but for 2M22 the sales still dropped 5% YoY, the sustainability of the sales deserves investors’ attention.

The one-month interbank HIBOR hit a new month high last week, Investors should pay attention to whether the aggregate balance of HKMA will drop further. At present, the aggregate balance has fallen to less than HK$80bn, the lowest since 2020. If it is further reduced to below HK$50bn, it may have a negative impact on investor confidence. The liquidity issues of non-SOEs developers have once again attracted attention. If investors speculate on further relaxation on the property market, it is advisable to focus on SOEs developers. Hang Seng index once fell below the 250 days SMA, however, after rebounding 800 points on Wednesday, it regained the 250 and 10 days SMA level. Although the economic data in China is improving significantly, we are worried about the sustainability of the performance. In addition, the US labor market is still strong, which makes the interest rate trend more uncertain. If the Hang Seng Index cannot rise above 20 days SMA (about 20,700 points), we expect Hang Seng Index to consolidate and trade between 19,500-20,700 points.

Telecommunications sector outperformed the market last week, but due to lack of more catalysts and the share prices have priced in most of the positives, we believe the upside to be limited. We expect that construction-related sectors will continue to benefit from the government’s effort to drive economic growth, construction-related stocks are expected to outperform the market in the near term.

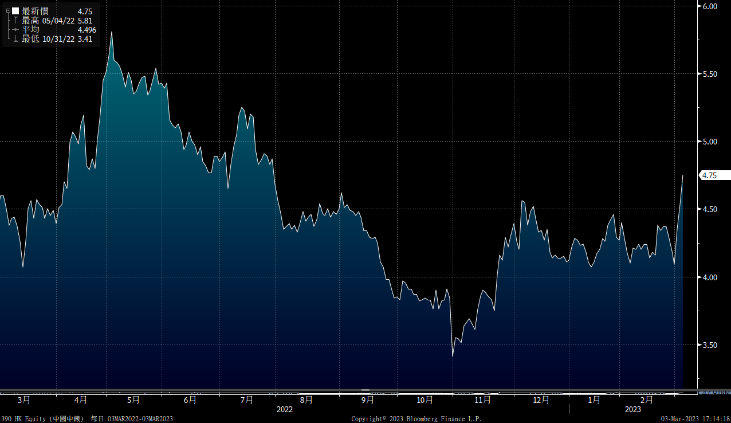

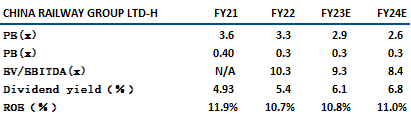

China Railway Group (390) is mainly engaged in infrastructure construction, design, and consulting services. For 9M22, the company’s revenue was CNY 850bn, +10.4% YoY, and its profit was CNY 23.016 bn, +11.5% YoY. For 2022, the new projects amounted to CNY 3.03 tn, +11.1% YoY.

Benefiting from the supportive policies for the property markets, the market expects that demand for infrastructure will improve significantly in 23E. In 2022, China’s fixed asset investment only increase 5.1% YoY. Under the low base and improved demand, the company’s new contracts are expected to achieve mid to high double growth. In addition, the company continues to expand into new business such as water conservancy and hydropower, clean energy, port channels, offshore wind power, pumped storage power, and water transfer projects etc. In which new orders for water conservancy and hydropower was +600% YoY during 9M22. We are optimistic about the company’s prospects. It is recommended to buy at HK$4.5, target at HK$5.1, stop loss at HK$4.25. Risks: The net profit margin is low, only 2.4%.

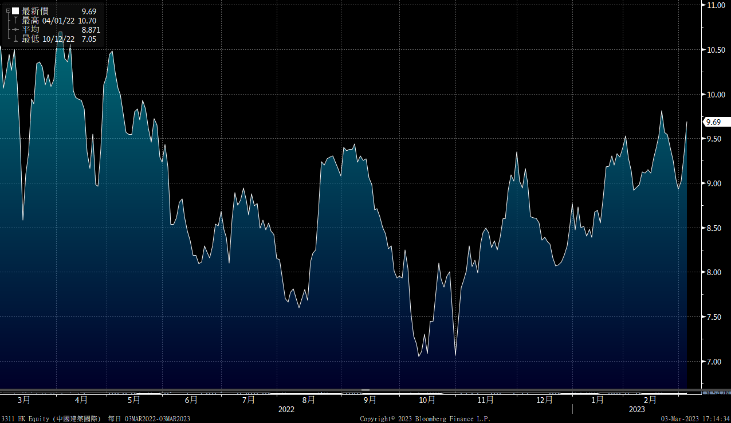

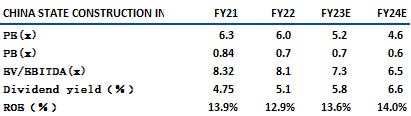

China State Construction (3311) is principally engaged in the construction business and is a leading company in China, Hong Kong and Macau. For 9M22, the company’s revenue was HK$73.41 bn, +38.9% YoY and the operating profit for the period was HK$9.8 bn, +17% YoY. And for 2022, the new contracts amounted to HK$160.7 bn, +15% YoY and achieved the target of HK$160bn.

Revenue from Hong Kong accounts for nearly 40% of the total revenue. We expect the company to benefit from the increasing construction demand in Hong Kong, including the “northern metropolitan” and the accelerated construction of public housing (average annual completion of public housing in Hong Kong during 2023-27 is about 21,100, vs 16,300 in 2014-22). For 23E, mgmt targets to have new projects of HK$180bn, +12.5% YoY. Mgmt reiterates the target of boosting ROE to 15% from 12.9% by 25E, backed by tech-driven construction of MiC (modular integrated construction), and BIPV (building-integrated photovoltaics). We are optimistic about the company’s prospects, and recommend investors to buy at HK$9.10, target at HK$10.2, stop loss at HK$8.6. Risk: Recovery in infrastructure investment is slower than expected.

HSI:

Source:Bloomberg

本周重要事件:

XINYI SOLAR (968 HK): NP in 22 dropped 22.4% YoY to HK$3.8bn |

China’s official PMI rose to 52.6 in February |

China’s non-manufacturing PMI rose to 56.3 |

BUD APAC (01876 HK): NP in 22 dropped 3.9% YoY to US$913mn |

TTI (669 HK): NP in 22 dropped 2% YoY to US$1.077bn |

BILIBILI-W (09626.HK): Net loss in 22 widens to CNY6.7B |

| Key events for next week: | |

|---|---|

|

03/07 |

WHARF REAL ESTATE INVESTMENT (1997) result, China import and export |

|

03/09 |

MTR CORPORATION (66), China CPI, PPI |

|

03/10 |

AIA GROUP (1299) results |

Sector performance:

| 1week performance(%) | |

|---|---|

|

Utilities |

0.6% |

|

Real estate |

2.4% |

|

Industrial |

2.9% |

|

IT industry |

4.0% |

|

Financial |

2.3% |

|

Energy |

2.4% |

|

Raw material |

2.4% |

|

Medical and health care |

3.5% |

|

Telecommunications |

6.5% |

|

Consumer discretionary |

3.0% |

|

Consumer staples |

2.3% |

Source:Bloomberg

Stock pick: China Railway Group (390)

Stock pick: China State Construction (3311)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓