PBOC stay accommodative, new bank loans in China jumped more than expected to a record of CNY 4.9 tn in January. While new home prices rose for the first time in a year, as the government stepped up support for the property sector. In addition, CSRC launched the trial program for real estate private equity investment fund to support the stable and healthy development of the real estate market, however, the impact is going to take time. China developers are going to announce their annual results and is not expected to have upside surprises, we believe sales performance to be the key for share price performance. “Hong Kong Budget 2023” announced a HK$5,000 consumption e-voucher to each HK permanent residents. Although it is not expected to have any material impact on the retail market, it is expected to support consumer sentiment. We expect neighbourhood retail mall operators, including Link REIT (823 HK) and Fortune Property (778 HK) to benefit.

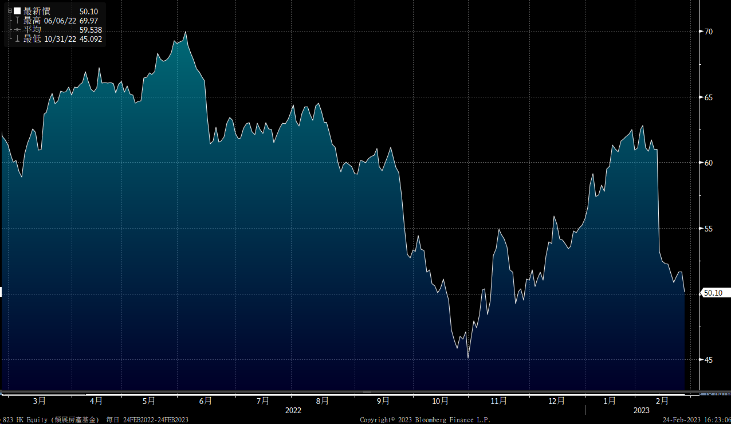

The aggregate balance of HKMA has fallen to less than HK$80bn, the lowest since 2020. Investors should pay attention to whether it will further drop to HK$50bn, as it may have a negative impact on investor confidence. It is now the peak season for result announcements, but some of the blue-chip companies missed market expectations, which have affected the overall performance of the Hong Kong market. The technical trend was weak with the Hang Seng Index staying below the 10-days and 20-days SMA. With concerns about US interest rate hikes and the global economic outlook, we expect investors to remain on the sidelines. We expect the Hang Seng Index to trade between 20,000 points to 21,200 points. The market will also focus on兩會 (NPC, CPPCC) which will be held on 4-5 March, and to see whether there will be measures to support the property market, infrastructure, and consumption sectors.

Benefiting from the HK$5,000 consumption e-voucher, we expect it to have a positive impact on sales in shopping malls. In addition, the stock prices of Link REIT (823) and Swire Properties (1972) have corrected significantly recently, which is believed to have reflected most of the negatives, share price rebound is expected.

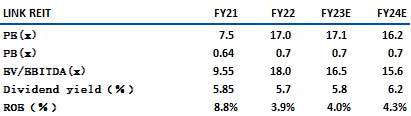

Link REITs (823 HK) has more than 130 investment projects in HK and 22 projects outside HK with portfolio value of ~HK$234bn. The company proposed a 1-for-5 rights issue (~30% discount) with expected gross proceeds of HK$18.8 bn, in which ~40%-50% will be used to repay debt, and it is expected to reduce its gearing ratio from nearly 27% to less than 20%. The remaining (~50%-60%) will be used to explore future investment opportunities, including retail, parking, office and logistics sectors in the Asia Pacific region.

We believe the share price has reflected the negative impact of the rights issue. Benefiting from the border reopening and normalization of economic activities (~ 60% of the company’s revenue comes from HK retail), we expect occupancy rate in HK retail to stay at high level (~97.5%) and the rental reversion rate to achieve mid to a high single digit increase. Moreover, Car park business can be the driver (accounting for ~20% of revenue). The monthly car park tariff has increased in 2H22 (mid-single digit), also two car park/car service centres acquired in 2021 have started contribution, revenue from car park rental is expected to have double-digit YoY growth. With the asset acquired in FY22 (HK$15 bn, or ~7% of portfolio value, including overseas offices, retails, and China logistics) starting contributions, together with revenue from HK continuing to recover, we expect DPU to have mid-single digit growth. We recommend investors to buy at $48.6, target $55.0, and stop loss at $46.0. Risk: Increasing interest rates may reduce the attractiveness of the company’s dividend yield.

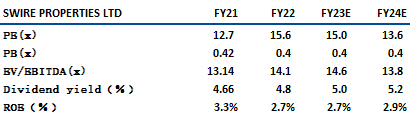

Swire Properties (1972 HK) is mainly engaged in property development and investment in Hong Kong and China, of which Hong Kong/Mainland accounted for 59% and 39% of the revenue. In 4Q22, the occupancy rate of the company’s overall office buildings in Hong Kong dropped from 97% to 96%, while the occupancy rate of retail properties in Hong Kong remained at 96%-100%. Although the company’s performance in the 4Q22 was under pressure, we expect the occupancy rate to improve as the relaxation of Covid measures in China and the improvement of consumer sentiment in China and Hong Kong.

Investment properties in China is expected to grow steadily with GFA in China growing from approximately 9.7 mn sq ft to 11.1 mn sq ft (around 2026). In Hong Kong, the company has a leading office portfolio of approximately 7 mn sq ft in Island East. Its “Two Taikoo Place” in Quarry Bay was completed in September 2022, with an occupancy rate of about 56%. With increasing occupancy rates, we are positive about the rental income. In terms of property development, the company is expected to launch ~1,800 units in 2023 (no new project launched in 22). We recommend investors to buy at $20.0, target $22.5, and stop loss at $19.0. Risk: The occupancy rate and rent per sqft of office buildings in Hong Kong are under pressure.

HSI:

Source:Bloomberg

Key events for the week:

The 1-year loan prime rate (LPR) was kept at 3.65%, the 5-year LPR was unchanged at 4.30%. |

HSBC (5 HK): FY22: Net profit up 17.6% YoY to US$14.8bn, beats expectation |

HSB (11 HK): FY22: Net profit -27% YoY to HK$10.17bn (est HK$13.39bn) |

TTI (669 HK): Accused by short sellers of exaggerating profits |

Stamp duty changes to help first-time buyers |

HKEX (388 HK): FY 22: Net profit dropped 20% YoY to HK$10.1bn |

BABA(9988): FY2Q23: Revenue +2% YoY to CNY247.76bn, est CNY245.18bn |

| Key events for next week: | |

|---|---|

|

02/27 |

CLP Holdings (2) Results, Xinyi Glass (868) Results, Xinyi Solar (968) Results |

|

03/01 |

China PMI, TTI (669) results |

|

03/02 |

Bilibili (9626) results |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

-1.6% |

|

Real estate |

-1.1% |

|

Industrial |

-0.8% |

|

IT industry |

-7.4% |

|

Financial |

-0.7% |

|

Energy |

0.6% |

|

Raw material |

-0.7% |

|

Medical and health care |

-2.4% |

|

Telecommunications |

0.4% |

|

Consumer discretionary |

-3.7% |

|

Consumer staples |

-2.0% |

Source:Bloomberg

Stock pick: Link REITs (823 HK)

Stock pick: Swire Properties (1972 HK)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓