According to the National Bureau of Statistics of China, the CPI for April increased by 2.1% YoY, which is the highest increase since December 2020. The increase is mainly due to the impact of the continuous rise in international commodity prices. The national CPI in April increased by 0.4% MoM, and increased by 2.1% YoY. The data showed that food prices increased by 0.9% MoM, which affected the CPI to rise by about 0.17pcts. The prices of potatoes, eggs, and fresh fruits rose by 8.8%, 7.1%, and 5.2%, respectively. As the production capacity of live pigs is gradually adjusted and the government’s frozen pork reserve collection and storage work is carried out in an orderly manner, the price of pork rose by 1.5% from a decrease of 9.3% last month. The price of fresh vegetables fell by 3.5% due to the increase in the supply of fresh vegetables. The average CPI from January to April increased by 1.4% compared to the same period last year.

China’s PPI fell by 3.6% YoY in April, which is the largest decline since May 2020 and greater than the market’s expectation of 3.3%. The PPI fell by 0.5% MoM in April. The prices of petroleum, coal, and other fuel processing industries fell by 2.3% MoM, while the prices of chemical raw materials and chemical product manufacturing industries fell by 1.1% MoM, affected by fluctuations in international crude oil prices. The prices of black metal smelting and rolling processing industries fell by 1.0% MoM, and the prices of cement manufacturing fell by 0.1% MoM, despite the overall sufficient supply of steel, cement, and other industries. The prices of coal mining and washing industries fell by 4.0% MoM, and the prices of non-ferrous metal smelting and rolling processing industries rose by 0.2% MoM, with copper smelting prices rising by 0.3% MoM and aluminum smelting prices rising by 0.1% MoM. As for the Hong Kong market, since it lacks upward momentum, we expect HSI to trade between 19,500-20,500 points.

According to the National Bureau of Statistics of China, the CPI for April increased by 2.1% YoY, which is the biggest increase since December 2020. The increase is mainly due to the impact of the continuous rise in international commodity prices. The national CPI in April increased 0.4% MoM, and had increased by 2.1% YoY. The data showed that food prices increased by 0.9% MoM, which caused the CPI to rise by about 0.17pcts. The prices of potatoes, eggs, and fresh fruits rose by 8.8%, 7.1%, and 5.2%, respectively. As the production capacity of live pigs is gradually adjusted and the government’s frozen pork reserve collection and storage work is being carried out in an orderly manner, the price of pork rose by 1.5% from a decrease of 9.3% last month. The price of fresh vegetables fell by 3.5% due to the increase in the supply. The average CPI from January to April increased by 1.4% compared to the same period last year.

China’s PPI fell by 3.6% YoY in April, which is the largest decline since May 2020 and greater than the market’s expectation of 3.3%. The PPI fell by 0.5% MoM in April. The prices of petroleum, coal, and other fuel for processing industries fell by 2.3% MoM, while the prices of raw materials for chemical products and chemical industries’ product fell by 1.1% MoM, affected by fluctuations in international crude oil prices. Despite the overall sufficient supply of steel, cement, and other industries, demand has been below expectations. The product prices of black metal smelting and rolling processing industries fell by 1.0% MoM, and the prices from cement manufacturers fell by 0.1% MoM. The prices of from coal mines and washed clean coal fell by 4.0% MoM, and the prices of non-ferrous metal smelting and rolling processing industries rose by 0.2% MoM, with copper smelting prices rising by 0.3% MoM and aluminum smelting prices rising by 0.1% MoM. As for the Hong Kong market, since it lacks upward momentum, we expect HSI to trade between 19,500-20,500 points.

The market expects the automotive sector to maintain a trend of moderate recovery this year, and the growth of exports may bring opportunities for some companies. Investors should pay attention to relevant companies.

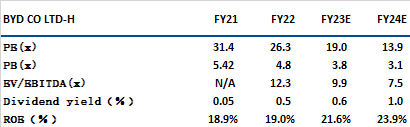

BYD Company Limited (1211.HK) reported Q1 results with revenue of Rmb120.2bn (+80% YoY) and net profit of Rmb4.1bn (+411% YoY). The strong revenue was mainly driven by a 89% YoY growth in auto sales. In Q1, BYD’s gross profit stood at Rmb19.2bn with a gross margin of 16.0%.

The company has its dominance in the China’s EV market (28% of the market in 2022). Its brand equity and scale of operation are expected to be its long-term competitive advantages in the upcoming market consolidation. Possible near-term catalysts are 1) a drop in lithium price, 2) better-than-expected volume growth, 3) increase in export sales. It is recommended to buy at HK$235.9, target at HK$274.8, and stop loss at HK$226.2.

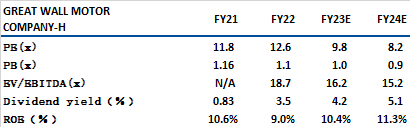

Great Wall Motor (2333.HK) overseas sales up 182% YoY in Apr. In Apr 23, GWM’s wholesale volume reached 93k units, an increase of 73% YoY due to a low base in the previous year. A record high of 22k units were sold outside China during the month, up 182% YoY whereas domestic sales stood at 71k units, a 6-year low excluding 2022 despite a 55% YoY increment.

According to the mgt, due to more promotions in Apr, GWM managed to effectively trim its inventory. In order to meet the new emission standard, the Mgt expects to clear all of its China 6a vehicles by the end of May. GWM is catching up with its peers in rolling out more EVs. Its EV sales now account for about 16% of its total. However, its ambitious sales target is 1.6mn units in 23E and GWM has only completed 20% of this already reduced target in 4M23. Its strong and lucrative overseas sales may offset the negative effect of the price war in China. It is recommended to buy at HK$9.5, target at HK$11.1, and stop loss at HK$9.1.

HSI:

Source:Bloomberg

Key events for the week:

China’s April PPI fell 3.6% YoY, worse than expected |

CPI rose 0.1% YoY in April, worse than expected |

Hua Hong (1347.HK) profit reached US$152 mn in 1Q23 +48% YoY |

Li Auto (2015.HK) net profit reached CNY900 mn in 1Q23 |

| Key events for next week: | |

|---|---|

|

05/16 |

Fixed assets estimates YoY; Retail Sales YoY |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

1.0% |

|

Real estate |

-4.9% |

|

Industrial |

-1.8% |

|

IT industry |

-1.9% |

|

Financial |

-2.2% |

|

Energy |

1.8% |

|

Raw material |

-10.5% |

|

Medical and health care |

-5.4% |

|

Telecommunications |

-2.9% |

|

Consumer discretionary |

-1.7% |

|

Consumer staples |

-3.5% |

Source:Bloomberg

Stock pick: BYD (1211.HK)

Stock pick: GWM (2333.HK)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓