The travel data during the Labor Day holiday Golden Week in mainland China has been released, and both the number of travelers and tourism revenue exceeded the same period in 2019. The Ministry of Culture and Tourism of China revealed that the recovery momentum of the cultural and tourism industry during this year’s Labor Day holiday was strong, and the market had been steady. According to the data center of the Ministry of Culture and Tourism, a total of 274 million domestic tourists traveled during the Labor Day holiday, +70.83% YoY, which had recovered to 119.09% of the same period in 2019. Domestic tourism revenue reached CNY148.05 bn, +128.90% YoY, which recovered to 100.6% of the same period in 2019.

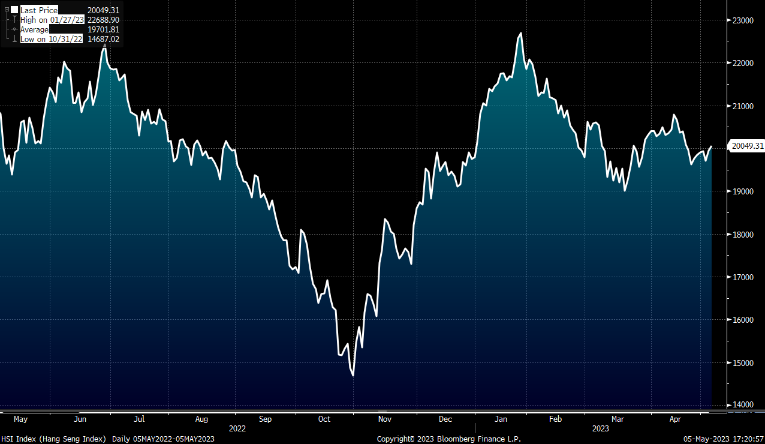

The Caixin China General Services PMI for April was 56.4, lower than expectation but still at a historical high. The supply and demand in the service sector were both robust, and the new order index fell slightly but remained significantly higher than the boom-bust line. The strong supply and demand also boosted employment in the service industry. The Caixin China Manufacturing PMI for April was 49.5, down 0.5pct from the previous month. The Caixin China Composite PMI for April was 53.6, down from the March high of 54.5. The operating costs of the service industry accelerated in April, with increased labor costs being the main reason for the rise in operating expenses. However, due to the need to attract and retain new orders, there is limited room for price hikes. As for the Hong Kong market, since it lacks upward momentum, we expect HSI to trade between 19,500-20,700 points.

The real estate policy relaxation and the lowering of mortgage rates are expected to further show effects, and real estate activities may gradually recover. Investors can pay attention to related companies in the industry.

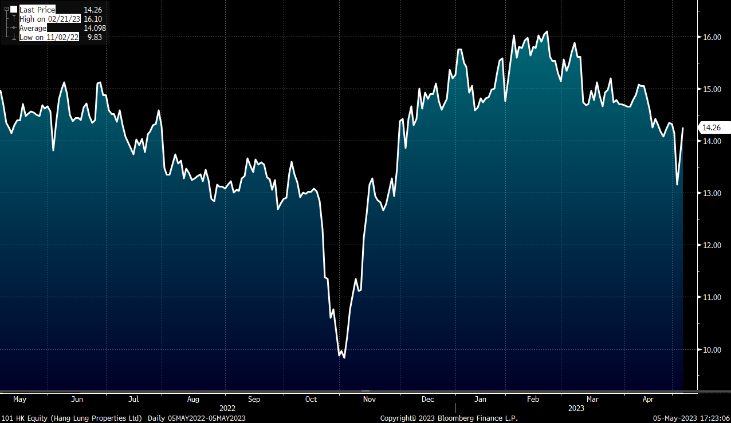

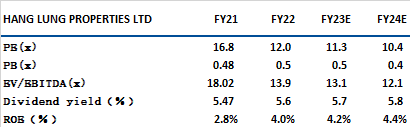

HANG LUNG PROPERTIES (101) FY22 revenue increased 0.3% YoY to HK$10,347mn and the underlying net profit dropped 4% YoY to HK$4,199mn. Tenants’ retail sales in Shanghai Plaza 66, Grand Gateway 66, and Wuxi Center 66 (accounting for ~30% of rev) during 1Q23 were up 16%-17% YoY. Despite the international border re-opening, tenants’ sales in luxury malls have remained solid. According to the mgmt, tenants’ sales in the three malls continue to have MoM improvements since Feb.

Mgmt targets to launch the remaining ~168 units (saleable value ~HK$1.5 bn) of The Aperture in 23E and the 10 unsold units of 23-39 Blue Pool Road (est >HK$ 300m each) in HK. Onshore luxury sales remain resilient, and the market expects luxury sales to have 15% -25% YoY growth in 23E. Based on (1) high-end customers being less affected by the economy, (2) the high stickiness for luxury brands, (3) luxury brands have reduced their price gap compare with offshore, together with the recovery of local tourism in China, Hang Lung Properties should continue to deliver solid results. It is recommended to buy at HK$13.8, target at HK$16.1, and stop loss at HK$13.3.

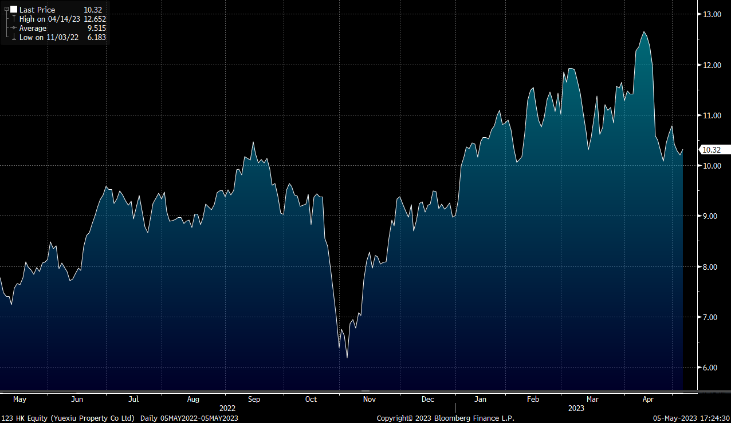

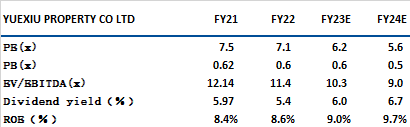

YUEXIU PROPERTY (123) contracted sales in 1Q23 +217.3% YoY (peers ave +~3% YoY) to CNY 43.8bn and accounted for ~33% of 23 sales target (CNY132bn). In Mar, the contracted sales amounted to CNY21bn, +257% YoY (peers +29.2%) or +53% MoM (peers +42%).

The land bank GFA amounts to ~28.5m s.qm of which 93% are in tier 1 and 2 cities. We believe an ample land bank with a top tier cities focus will help in supporting sales. YP remained in the “green” category with net gearing of ~62.7% and cash to short-term debt ~2.23X. The average borrowing cost dropped from 4.26% in 21 to 4.16% in 22. YUEXIU PROPERTY (YP) proposed to raise ~HK$8,360 mn in a 30 for every 100 shares rights issue. The net proceeds from the rights will be used for further investment in the Greater Bay Area (accounted for ~48% of contracted sales in FY22), the Eastern China Region (accounted for 34% of contracted sales in FY22) plus working capital. It is recommended to buy at HK$10.0, target at HK$11.7, and stop loss at HK$9.6.

HSI:

Source:Bloomberg

Key events for the week:

Aoyuan Healthy (3662.HK) profit declined 72% YoY in 1H22 |

Beigene (6160.HK) loss was CNY2.4 bn in 1Q23 |

BUD APAC (1876.HK) profit reached US$2970 mn in 1Q23 |

Hongjiu Fruit (6689.HK) revenue up 50% YoY in 1Q23 |

| Key events for next week: | |

|---|---|

|

05/09 |

Sum of goods import and export value |

|

05/11 |

CPI MoM |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

2.3% |

|

Real estate |

0.7% |

|

Industrial |

1.3% |

|

IT industry |

0.2% |

|

Financial |

2.4% |

|

Energy |

0.2% |

|

Raw material |

2.8% |

|

Medical and health care |

0.5% |

|

Telecommunications |

1.6% |

|

Consumer discretionary |

0.1% |

|

Consumer staples |

-0.7% |

Source:Bloomberg

Stock pick: HANG LUNG PROPERTIES (101)

Stock pick: YUEXIU PROPERTY (123)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓