In April, the total retail sales of consumer goods in China reached CNY3.49tn, +18.4% YoY, which was lower than the market’s expectation of 21.9%. The retail sales of consumer goods excluding automobiles were CNY3.13tn, +16.5% YoY. In 4M23, the total retail sales of consumer goods reached CNY14.98tn, +8.5% YoY, and the retail sales of consumer goods excluding automobiles were CNY13.57tn, +9.0% YoY. In April, retail sales reached CNY3.12tn, +15.9% YoY, and catering revenue was CNY375.1bn, +43.8% YoY. In 4M23, retail sales were CNY133.95tn, +7.3% YoY, and catering revenue was CNY1.59tn, +19.8% YoY.

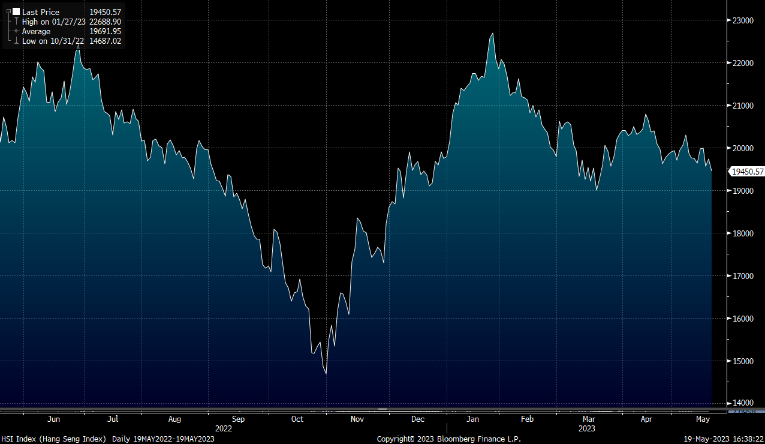

In 4M23, the total online retail sales in China reached CNY4.41tn, +12.3% YoY. The online retail sales of physical goods were CNY3.72tn, +10.4% YoY, accounting for 24.8% of the total retail sales. In 4M23, the national real estate development investment was CNY3.55tn, +6.2% YoY. Among that, residential investment was CNY2.71tn, -4.9% YoY. In 4M23, the sales of commercial properties was 376.36mn square meters, -0.4% YoY, and the sales value of commercial properties reached CNY3.98tn, +8.8% YoY. The sales value of residential properties increased by 11.8% YoY. As for the Hong Kong market, since it lacks upward momentum, we expect HSI to trade between 18,500-20,000 points.

In terms of industry, due to the low base last year, the consumer sector has recovered faster this year, and investors are recommended to pay attention to consumer-related companies.

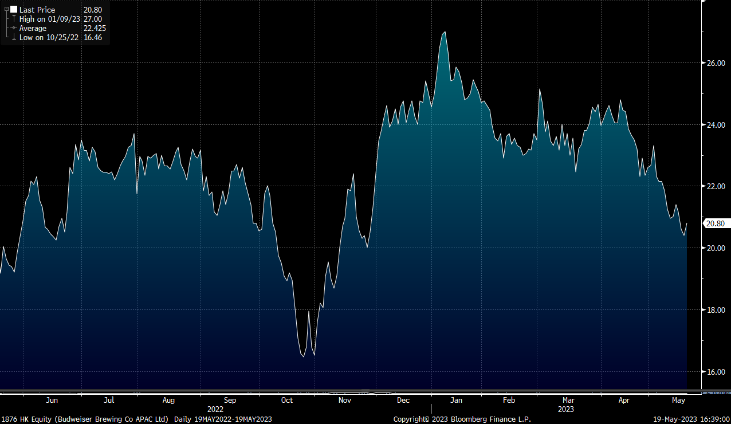

Budweiser APAC (1876.HK) reported revenue of US$1.70bn in 1Q23, +12.9% YoY whereas total volume sold was 9.1% higher YoY to about 22.1mn hl, mainly driven by the recovery in the China market and continuous growth in South Korea and India. The company’s volumes and revenue in China increased by 7.4% and 10.9% respectively, all grew to above pre-pandemic levels.

In 1Q23, the company’s normalized EBITDA increased by 10.4% YoY to US$580mn. The results came in slightly above the consensus. South Korea and India saw double-digit growth in both volumes and revenue, and the Mgt expect the strong momentum in South Korea and India to continue with increasing demand and premiumization. Despite an 11.1% YoY incremental increase to the company’s gross profit to US$854 mn in 1Q23, GPM had been eroded further by another 81 bps to 50.2% (vs 51.0% for 1Q22 and 52.8% for 1Q21), as the cost of sales rose by 14.8%. The Mgt remain highly optimistic on the premiumization potential of the Asian market in the longer term. It is recommended to buy at HK$20.2, target at HK$23.5, and stop loss at HK$19.3.

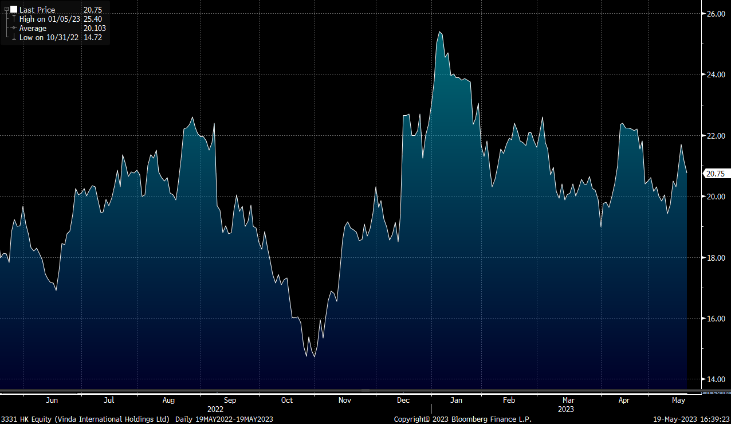

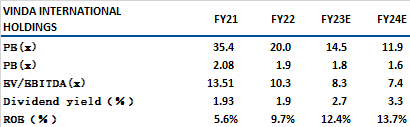

Vinda International Holdings Limited (3331.HK) posted a record high 1Q23 revenue of almost HK$5.00bn (+9% YoY, +16% YoY at constant FX rates) where contribution from China reached HK$3.93bn (+13% YoY, +22% at constant FX), mainly driven by the phenomenal growth in the E-commerce channel, which contributed to about HK$2.08bn in revenue with a 34% growth rate.

In Q1, Vinda’s tissue sales went up by 11% YoY to HK$4.07bn whereas sales for personal care products came in steady at HK$898mn. Per the mgt, Vinda’s premium tissue now accounts for about 43% of total tissue sales, up by 5% YoY or translating into a revenue growth of 25%. However, the growth of the high-hoped personal care products was weaker than expected. GPM was up 3 pct QoQ thanks to lower pulp prices. Vinda’s Q1 GPM edged up by 3 pct QoQ to 25.2%, benefiting from the pulp price drop. The mgt expects that the cost will continue to drop in the next three quarters if pulp price continues its downward trend. It is recommended to buy at HK$20.1, target at HK$23.4, and stop loss at HK$19.3.

HSI:

Source:Bloomberg

Key events for the week:

Retail sales of consumer goods in China increased by 18.4% in April, worse than expected |

The growth rate of national fixed asset investment in the 4M23 fell to 4.7%, worse than expected |

MINOSO (9896.HK) profit reached CNY470 mn in 1Q23 +382% YoY |

ZTO EXPRESS (2057.HK) net profit reached CNY1.67 bn in 1Q23 |

| Key events for next week: | |

|---|---|

|

05/27 |

Operating profits: Cumulative |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

-2.0% |

|

Real estate |

-3.8% |

|

Industrial |

-1.3% |

|

IT industry |

-0.7% |

|

Financial |

0.0% |

|

Energy |

0.7% |

|

Raw material |

-1.3% |

|

Medical and health care |

-4.3% |

|

Telecommunications |

-0.4% |

|

Consumer discretionary |

-1.6% |

|

Consumer staples |

-1.0% |

Source:Bloomberg

Stock pick: Budweiser APAC (1876.HK)

Stock pick: Vinda (3331.HK)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓