In June, the total retail sales of consumer goods reached 4.1 trillion yuan, a YoY increase of 2.0%, lower than expectations. The retail sales of consumer goods other than motor vehicles reached 3.6 trillion yuan, up 3.0%. In terms of consumption patterns, the spending in catering was 460.9 billion yuan, up 5.4%, while retail goods reached 3.6 trillion yuan, an increase of 1.5% YoY. Among that, cosmetics, household appliances and audio-visual equipment, and cultural and office supplies decreased by 14%、7.6% and 8.5%, respectively. The YoY growth rate of Grain, Oil and Food surpassed 10%. From January to June, the total retail sales of consumer goods were 24 trillion yuan, a YoY increase of 3.7%, while the retail sales of consumer goods other than motor vehicles reached 21 trillion yuan, up 4.1%.

In June, the total value added of industrial enterprises of designated size grew by 5.3% YoY. In terms of sectors, the value added of mining increased by 4.4% YoY, manufacturing went up by 5.5% and the production and supply of electricity, thermal power, gas and water grew by 4.8%. In terms of industries, in June, the value added of 35 of the 41 major industries kept their YoY growth. Chemical raw materials and chemical products manufacturing, non-ferrous metal smelting and rolling processing industry, railway, shipbuilding, aerospace and other transportation equipment manufacturing industries, computer, communications and other electronic equipment manufacturing were the main drivers, up 9.2%、10.2%、13.1% and 11.3% YoY respectively. In terms of the Hong Kong stock market, the Hang Seng Index may lack upward momentum in the near term. It is expected to fluctuate between 16,900 – 17,900 points.

In terms of industry, as mainland banks have maintained robust momentum of balance sheet expansion and offer attractive dividend yields, investors can pay more attention to relative companies.

China Construction Bank (939.HK)’s revenue in Q1 amounted to RMB200.9 billion, a YoY decrease of 3%. Net profit stood at RMB86.9 billion, a YoY decrease of 2.5%. At end-March, CCB’s total assets/loans/deposits rose 7.5/11.1/6.9% YoY, suggesting a slowdown in the pace of balance sheet asset expansion. In 1Q24, new loans were chiefly corporate loans. CCB continued to exert its efforts in the “Five Major Chapters”. At the end of March, loans to sci-tech enterprises, green loans, and inclusive finance loans reached RMB1.80 trillion, 4.45 trillion, and 3.28 trillion respectively. The (NIM) for 1Q24 contracted 13bp vs 2023 to 1.57%, potentially due to re-pricing.

Asset quality remained solid in 1Q24. Its NPL ratio was 1.36% at end-March 2024, down from 1.37% at end-December 2023. Its allowance to NPLs reached 238.2% in 1Q24 against 239.9% in 2023. What’s more, CCB’s dividend yield is attractive. A total dividend of RMB0.4 share was declared in FY23, with a yield of 8.2%. It is recommended to buy at HK$ 5.15, target at HK$6.00, and stop loss at HK$4.95.

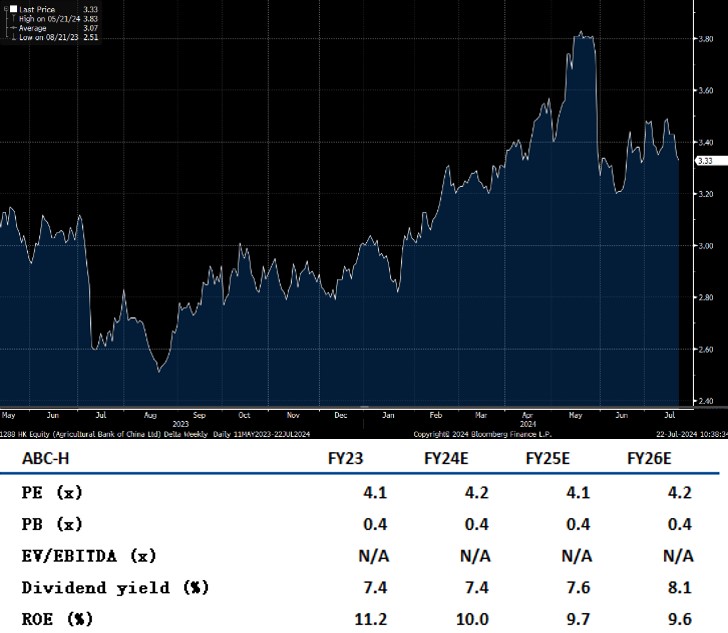

Agricultural Bank of China (1288.HK)’s revenue in Q1 amounted to RMB186.1 billion, a YoY decrease of 1.70%. Net profit stood at RMB70.3 billion, a YoY decrease of 1.63%. At end-March, ABC’s total assets/loans/deposits rose 14.5/12.9/12.2% YoY. ABC enjoyed the fastest growth in total assets among big banks, suggesting the robust momentum in balance sheet expansion.

The (NIM) in 1Q24 contracted 16bp vs 2023 to 1.44%, mainly due to re-pricing for existing loans, adjustments to mortgage rates, and another cut in over 5Y LPR. At end-March, the proportion of demand deposits fell by 1ppt vs end-2023 to 41.9%. YoY growth in ABC’s net interest income in 1Q24 came to -0.7%, up 2.3ppt compared to 2023. At end-March, the balance of loans/deposits at county levels grew 7.1/7.2% YoY compared to the end of 2023, suggesting the steady expansion of county-level business. At end-March, the balance of loans to manufacturing sector/green credit/inclusive loans expanded 12.7/18.9/22.6% YoY compared to the end of 2023, implying the lender’s stepping up efforts to prop up the real economy. ABC pays stable dividends and has an attractive dividend rate. The total dividend in FY23 amounted to RMB0.23 per share, with a yield of nearly 7.6%. It is recommended to buy at HK$3.25, target at HK$3.75, and stop loss at HK$3.10.

HSI:

Source:Bloomberg

Key events for the week:

- Public Financial (626.HK) turned from interim profit to a loss of HK$34.49 million

- Connect Optical (2276.HK) expected interim profit to increase by more than 30%

- Giordano (709.HK) expected interim profit of HK$110 million to HK$130 million

- Lee & Man Paper (2314.HK) expected interim profit to rise 1.2 times YoY

| 下周重要事件 | |

|---|---|

|

07/22 |

HK CPI |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

0.5% |

|

Real estate |

-3.5% |

|

Industrial |

-2.7% |

|

IT industry |

-3.2% |

|

Financial |

-2.3% |

|

Energy |

-2.8% |

|

Raw material |

-4.1% |

|

Medical and health care |

-8.8% |

|

Telecommunications |

0.1% |

|

Consumer discretionary |

-2.6% |

|

Consumer staples |

-3.6% |

Source:Bloomberg

Stock pick: China Construction Bank (939.HK)

Source:Bloomberg

Stock pick: Agricultural Bank of China (1288.HK)

Source:Bloomberg

Analyst: CHAN Ka Kin (CE Number BHS185)

Disclosure of Interest

Neither the analyst(s) preparing this report nor his associate has any financial interest in; or serves as an officer of the listed corporation covered in this report. The remuneration of the analyst(s) is not directly or indirectly related in any way to the particular opinions or views expressed in this report.