According to the National Bureau of Statistics, the national consumer price index (CPI) in June rose by 0.2% YoY and fell by 0.2% MoM. Excluding food and energy prices, core CPI rose by 0.6% YoY, maintaining a moderate increase. In June, as supply was generally sufficient, the CPI fell MoM, with stable YoY growth. Food prices fell by 0.6% MoM. As some seasonal fruits, vegetables and aquatic products were put on the market in batches, the prices of fresh vegetables, potatoes, fresh fruits, and shrimps and crabs fell by 7.3%, 4.8%, 3.8% and 2.4% MoM, respectively. The price of pork rose by 11.4% month-on-month. Non-food prices fell by 0.2% MoM, the same as last month. Affected by the “618” shopping promotions, the decline of automobiles, household appliances, and cultural and durable consumer goods prices were in the range of 0.8% to 1.3%. As the summer vacation approaches, the prices of transportation rental fees and air tickets rose by 6.4% and 2.5% MoM respectively.

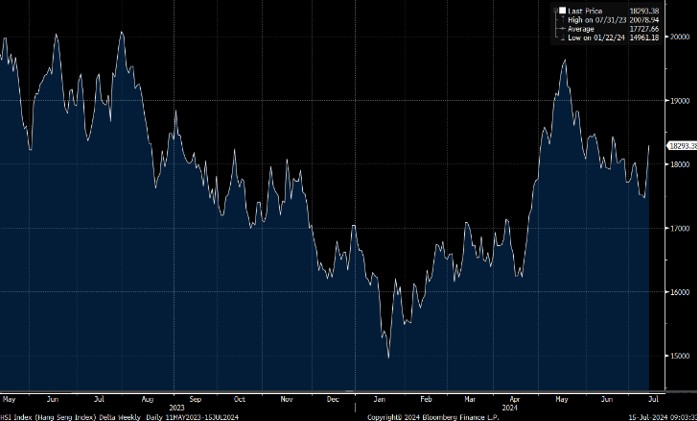

PPI fell by 0.8% YoY in June, about 0.6 ppt less than the previous month. Among that, the price of means of production fell by 0.8%, the decline had narrowed by 0.8 ppts. The price of means of livelihood fell by 0.8%, the decline was the same as last month. The prices in coal mining and washing and selecting industry fell by 1.6%, while non-metallic mineral products dropped by 6.9%. The price of ferrous metal smelting and processing declined by 2.1%, and that of agricultural and sideline products processing industry was down by 2.2%. The price of computer communication and other electronic equipment manufacturers declined by 2.1%. In terms of the Hong Kong stock market, the Hang Seng Index may lack upward momentum in the near term. It is expected to fluctuate between 17,600-18,700 points.

In terms of industry, as there are still many uncertainties in the HK stock market, investors can pay attention to high dividend stocks with stable performance.

CK Infrastructure(1038.HK) net profit in FY23 reached HK$8 billion, representing a 4% YoY growth. Profit contribution from Power Assets was HK$2.1 billion, representing a growth of 6%, accounting for 26% of total net profit. Net profit from the United Kingdom business stood at HK$3.0 billion in 2023, the same as FY22. In Australia, net profit decreased by 6% YoY to HK$1.8 billion, mainly due to weak currency exchange and a lower contribution arising from the regulatory resets for Australian Gas Networks (“AGN”) and Multinet Gas Networks. Net profit from Canada market increased 5% YoY to HK$600 million. In Continental Europe, net profit declined by 19% YoY to HK$535 million, due to the negative impact caused by a fire at the Rozenburg plant of Dutch Enviro Energy in September 2023.

The company declared a final dividend of HK$1.85 per share. Together with the interim dividend of HK$0.71 per share, the total dividend per share in 2023 was HK$2.56, up 1.2% YoY. This represents 27 consecutive years of dividend growth since listing. The dividend yield in FY23 stood at 5.5%. It is recommended to buy at HK$48.00, target at HK$54.00, and stop loss at HK$44.50.

China Resources Power(836.HK)’s net Profit in FY23 amounted to HK$11 billion , representing an YoY increase of 56.2%. Core profit from renewable energy business stood at HK$9.7 billion, up 12% YoY. Thermal power business turned from loss to a profit of HK$3.6 billion. In FY23, attributable operational generating capacity of 59,764MW, of which, thermal power amounted to 37,167MW, accounting for 62.2% of total. The attributable operational generation capacity of wind, photovoltaic and hydro power projects amounted to 22,597MW, accounting for 37.8% of total capacity, representing a YoY increase of 5.5 percentage points. During the year, the total net generation volume of the Group’s consolidated power plants amounted to 193,265GWh, up by 4.7% YoY. Net generation volume of wind farms and photovoltaic power stations increased by 12.4% and 111.8%, respectively, while net generation volume of consolidated thermal power plants increased by 2.3% YoY.

The company declared a final dividend of HK$0.587 per share in FY23. Together with the interim dividend of HK$0.328 per share and the special dividend of HK$0.5 per share, the full-year dividend came in at HK$1.415 per share, with a payout ratio of 62% and a dividend yield of 6%.

It is recommended to buy at HK$22.00, target at HK$24.50, and stop loss at HK$20.00.

HSI:

Source:Bloomberg

Key events for the week:

- Red Star Macalline (1528.HK) expects interim losses of up to nearly RMB1.6 billion

- Ganfeng Lithium (1772.HK) expects interim losses of up to RMB1.3 billion

- China Shenhua (1088.HK) expects interim profit to fall by up to 13.8% YoY

- Haitong Securities (6837.HK) expects interim profit to fall by up to 76% YoY

| Key events for next week: | |

|---|---|

|

07/15 |

China’s industrial added value above designated size in June |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

0.05% |

|

Real estate |

2.89% |

|

Industrial |

-0.26% |

|

IT industry |

4.74% |

|

Financial |

1.96% |

|

Energy |

-4.65% |

|

Raw material |

-1.31% |

|

Medical and health care |

0.79% |

|

Telecommunications |

0.92% |

|

Consumer discretionary |

3.53% |

|

Consumer staples |

2.62% |

Source:Bloomberg

Stock pick: CK Infrastructure(1038.HK)

Source:Bloomberg

Stock pick: China Resources Power(836.HK)

Source:Bloomberg

Analyst: CHAN Ka Kin (CE Number BHS185)

Disclosure of Interest

Neither the analyst(s) preparing this report nor his associate has any financial interest in; or serves as an officer of the listed corporation covered in this report. The remuneration of the analyst(s) is not directly or indirectly related in any way to the particular opinions or views expressed in this report.