China’s March Caixin (PMI) was 50, lower than the expected of 51.4, which showed signs of a weakening economic recovery and the revenge spending after Covid may not be sustainable. China’s economy is expected to face more downward pressure. HK property market has improved, new home sales in HK during Mar 23 amounted to HK$ 18.6bn, +174% MoM. We expect the momentum to continue due to gradual economic recovery in HK and China, improvement in buyer confidence and the expectation of interest rate peaking in 1H23. Sino Land (83HK), with a net cash position, is expected to outperform peers. The Hong Kong dollar weakened against the US dollar and the aggregate balance of HKMA dropped below US$70bn, which may negatively affect the investment sentiment and limit the performance of Hong Kong market.

According to market data, Saudi Arabia and other OPEC+ members are to reduce oil production by 1.6 million barrels per day in May. As the market was surprised by the sudden production cut, oil prices went up to over US$80 a barrel. Market expects the oil price to rise to US$90-95 dollars per barrel by the end of the 2023E. Although the recovery of China’s economy may be slower than expected, and the US banking liquidity issue may have a negative impact on the global economy, the rise in oil prices may increase global inflationary pressures and make the Fed’s interest rate moves more uncertain. The investment market is expected to be more volatile. For the Hong Kong market, although the Hang Seng Index is above 20,000 points, it lacks upward momentum. Technically, the Hang Seng Index sees resistance at around 20,500 (50 days SMA). We expect the Hang Seng Index to trade between 19,500-20,600 points.

Investors are looking forward to the performance of tourism and consumption during “5/1” ” holiday. Given the lack of investment themes, the retail sector is worth paying attention to in the short term.

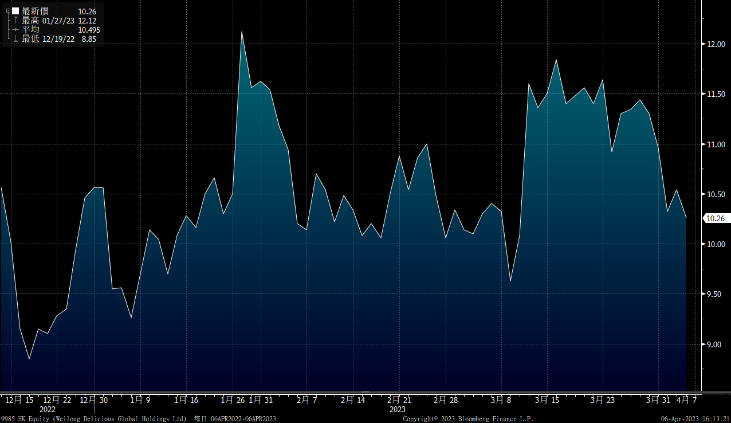

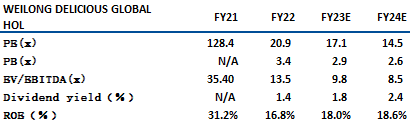

WEILONG (9985) is a leading spicy snack food company in China. Weilong’s revenue in FY22 was CNY4.63 bn, among which seasoned gluten products dropped 6.8% YoY, while vegetable and soybean products increased 1.8% and 1.0% respectively. The volume of seasoned gluten products, vegetable and soybean products were down 28.5%, 10.5% and 63.8% due to ASP hike in. Core net profit was CNY913.1 mn, +0.6% YoY and GP margin increased 4.9ppt to 42.3%.

Weilong’s GPM increased to 42.3% in FY22, vs 37.4% in FY21. In terms of products, GPM of seasoned gluten, vegetable and soybean products were 39.9%, 46.8% and 37.2% respectively. Mgmt expects to improve GPM by increasing the proportion of vegetable products in 2023. The company currently has more than 1,840 offline distributors in China and 40 distributors in overseas markets, covering more than 570,000 retail outlets. In the future, the company will actively expand its overseas markets. In 2022, revenue from overseas markets reached CNY65.5 mn, +230.7% YoY, accounting for 1.58% of Weilong’s total sales (vs 0.41% of total sales in 2021). We expect the revenue to have CAGR of 15% during 23-25E. It is recommended to buy at HK$9.9, target at HK$11.1, stop loss at HK$XX. Risks: food safety issues and unfavorable raw materials prices.

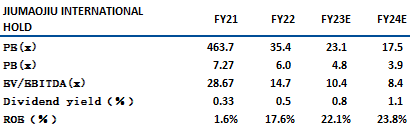

Jiumaojiu (9922 ) is principally engaged in restaurant operations with the brands of Jiu Mao Jiu, Tai Er etc. As of end of 2022, the company operated 475 restaurants, in which 77 restaurants were Jiu Mao Jiu and 384 were Tai Er. In 2022, company’s revenue was CNY 4 bn, -4.16% YoY, core net profit was CNY69.34mn, -81.8% YoY.

The store number of Jiumaojiu decreased by 8.4% to 76 in 2022, due to the closures of some loss-making stores. However, the number of Tai Er increased by 29.1% to 452, and Song Hot Pot opened 9 new stores to 18 stores in 2022. As Song Hot Pot has higher Seat turnover rate and average spending per customer than other bands, and mgmt expects to add 15-20 new stores in 23E, we believe this can help in driving the results. With the gradual recovery of economic activities, we expect the seat turnover rates to recover to pre-Covid level of ~4 times/day from current ~2.6 times/day. In addition, due to the low base, there is a big potential for the improvement in the company’s profitability. It is recommended to buy at HK$17.5, target at HK$19.6, stop loss at HK$16.5, Risk. slow economic growth may be unfavorable to food consumption.

HSI:

Source:Bloomberg

Key events for the week:

China Mar Caixin PMI was 50, below expectation of 51.4 |

Vanke (2202 HK): Contracted sales in 1Q23 were CNY 101.38 bn, -4.8% YoY |

| Key events for next week: | |

|---|---|

|

04/11 |

CPI、PPI |

|

04/13 |

Import and export value |

Sector performance:

| (%) | |

|---|---|

|

Utilities |

-1.9% |

|

Real estate |

0.5% |

|

Industrial |

-1.8% |

|

IT industry |

0.6% |

|

Financial |

0.5% |

|

Energy |

4.1% |

|

Raw material |

2.3% |

|

Medical and health care |

-0.3% |

|

Telecommunications |

5.5% |

|

Consumer discretionary |

-0.5% |

|

Consumer staples |

0.4% |

Source:Bloomberg

Stock pick: WEILONG (9985 HK)

Stock pick: Jiumaojiu (9922 HK)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓