China’s new loans in March was CNY 3.89 tn, higher than the expectation of CNY 3.3tn and CNY1.8 tn in Feb. In 1Q23, the new loans in China amounted to CNY10.3 tn, up CNY2.27 tn YoY, reflecting the still abundant liquidity. However, CPI in March was only +0.7% YoY, lower than the expected of 1% and PPI also fell 2.5% YoY. The data may reflect that domestic demand is still weak, and investors cannot be too optimistic about the economic growth and the corporate profitability, which will limit the performance of China and Hong Kong stock markets.

Hong Kong’s catering revenue during the Easter holiday fell by 15% to 20% compared with just after the relaxation of Covid measures, and local retail consumption also recorded a drop of nearly 10%-20%. We attribute to the weak consumption sentiment, locals traveling abroad and tourist from China only recovering to less than 40% of pre-Covid levels. Although the first batch of consumption vouchers will be distributed on the 16th April and is expected to boost consumer sentiment, the scale of the consumption vouchers has decreased by 50% YoY. As the local economy is still under pressure, we do not expect local catering and retail enterprises to perform well in the near future. Inflationary pressures in the U.S. eased and the market predicts that the probability of a 0.25% interest rate hike in May is about 70%, while Fed will start cutting rates in 2023. Regarding the Hong Kong market, although the Hang Seng Index is above 20,000 points, it lacks upward momentum. We expect the Hang Seng Index to trade between 19,500-20,500 points.

Raw material and Medical and health care sectors outperformed the market. As China will have “5/1” holiday soon, which is expected to support auto sales, the auto related sectors are worth paying attention to.

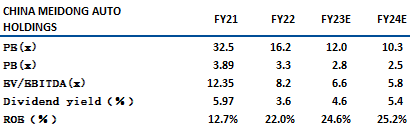

Meidong(1268) is principally engaged in 4S dealerships in China. In 2022, Meidong achieved revenue of CNY 28,654mn, +22% YoY and net profit of CNY 521mn, -55% YoY, mainly due to weaker auto market in 2022. Moreover, Meidong’s gross margin dropped 3 pct to 8.8%, the lowest since 2013. As of the end of 2022, company operated a total of 76 outlets, in which 16 were Porsches and 27 were BMWs.

Meidong is one of the largest Porsche dealers in China. In 2022, Meidong sold 67,871 vehicles, +10% YoY, incl. 11,790 Porsche, +107% YoY and 23,611 BMW, -5% YoY. Per mgmt, current foot traffic has improved recently and mgmt expects the recovering foot traffic to transfer to revenue soon. In 2M23, Porsche sales in China increased 20% YoY to 13,758 units (+11/14% compared with 2M21/2M19). We expect the ultra-luxury brand to benefit from China’s recovery in 2023. It is recommended to buy at HK$14.4, target at HK$16.2, stop loss at HK$13.5. Risk: More fierce than expected price war.

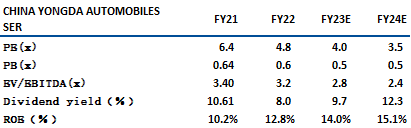

YONGDA AUTOMOBILES (3669) is principally engaged in the sale of automobiles and provision of after-sales services, provision of automobile operating lease services, provision of proprietary financing services, distribution of automobile insurance products and automobile financial products in China. In 2022, Yongda reported revenue of CNY72,024mn, -8% YoY and net profit of Rmb1,425mn, dropping 43% YoY mainly due to gross margin dropping from 10.8% in 2H21 to 8.1% in 2H22. As of the end of 2022, the company operated a total of 263 outlets, in which 62% were luxury brands, 19% were mid-to-high-end brands, 14% were independent new energy brands, while many of the 4S stores were Porsche, BMW, Audi etc.

In 2022, new car sales revenue dropped 9% to CNY 58,192mn, and vehicle sales gross margin declined 0.9 pct to 2.3%, mainly due to intensifying auto market competition in 2H22. However, mgmt. highlighted the pre-owned car segment and EV growth that could support future results, together with the promotion activities in some cities that might support sales. As the dividend is around 8%, it is recommended to buy at HK$5.0, target at HK$5.6, stop loss at HK$4.7. Risk: The auto sales in China remaining weak compared to 2022.

HSI:

Source:Bloomberg

Key events for the week:

China’s automobile sales volume +9.7% to 2.451mn units |

China’s new loans in March was CNY 3.89 tn |

CPI in March +0.7% YoY |

PPI in March -2.5% YoY |

PING AN (2318 HK): 1Q23 Premium incomes +5.6% YoY to CNY260.159bn |

| Key events for next week: | |

|---|---|

|

04/18 |

Fixed assets investment, GDP, Retail Sales, Industry value added, Electricity Generation |

Sector performance:

| 1 week performance(%) | |

|---|---|

|

Utilities |

2.8% |

|

Real estate |

3.8% |

|

Industrial |

2.4% |

|

IT industry |

-3.4% |

|

Financial |

2.0% |

|

Energy |

2.7% |

|

Raw material |

12.4% |

|

Medical and health care |

11.6% |

|

Telecommunications |

2.0% |

|

Consumer discretionary |

0.5% |

|

Consumer staples |

-0.4% |

Source:Bloomberg

Stock pick: Meidong(1268 HK)

Stock pick: Yongda (3669 HK)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓