The data of ADP National Employment report were worse than expected. In March, the private sector hiring rose by just 145,000, down from 261,000 in February and below the estimate of 210,000. In 1Q23, the average monthly hiring was 175,000, suggesting a cooling labor market. In addition, the U.S. ISM non-manufacturing index fell from 55.1 in February to 51.2 in March, lower than market expectations of 54.5 and was the lowest in three months. The above data reflected that the U.S. economy might be slowing, which could have a negative impact on future corporate earnings and U.S. stock performance.

The market continues to focus on the Fed’s stance on interest rate hike. According to market data, the probability of the Fed increasing the interest rate by 0.25% in May is over 80%. OPEC and other countries will reduce oil production which may increase the upward pressure on raw materials cost and inflation and making interest rates in the U.S. more uncertain. According to market data, investors’ positions in U.S. stocks are at an 18-year low, reflecting that investors are not optimistic about the prospects of U.S. stocks. However, if U.S. stocks remain strong in the near term, investors may need to reinvest into the stock market. Although the U.S. economic outlook and interest rate trends are still uncertain, the technical trend of the S&P 500 index is still strong and may trigger more capital inflows. We expect the S&P 500 index to trade between 3,800 points and 4,300 points.

The market expects limited room for the US to raise rates. We expect technology stocks to have revaluation potential and to outperform the market in the near term.

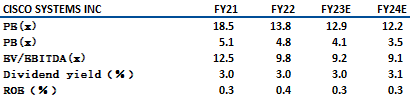

Cisco (CSCO) is one of the world’s largest network equipment supplier and software company. In FY2Q23, Cisco’s revenue was US$13.59 bn, higher than market expectations of US$13.43 bn, net profit was US$2.77 bn -7% YoY.

The company announced an update to its AppDynamics cloud software and disclosed a restructuring plan that includes adjustments to its real estate portfolio. Looking forward, the company expects the order on hand to double in FY23E when compared to normal condition, and the momentum to persist into FY2024. Mgmt expects revenue in the FY3Q23 to increase 11%-13% YoY, which is higher than the market expectation of 5.8%, while the revenue in FY23E to increase 9% to 10.5% YoY, which is also higher than market expectation of +5.7% YoY. As the mgmt has confidence in the future performance, it is recommended to buy at US$50.0, target at US$56.0, and stop loss at US$47.0.

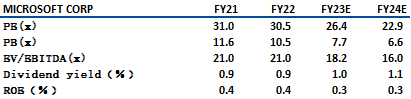

Microsoft (MSFT) develops and licenses consumer and enterprise software. The company’s revenue in 2Q23 was US$52.75 bn (+2% YoY), but lower than the market’s estimate of US$52.93 bn. The company’s net profit was US$16.43 bn, -12.5% YoY. However, the company’s cloud business performed well with revenue +22% YoY to US$27.1 bn.

Microsoft will deploy OpenAI programs in Azure, including GPT, DALLE, and Codex programs. It will also be OpenAPI’s exclusive cloud provider. After the introduction of ChatGPT technology, it will improve the search results’ matching. In addition, the latest artificial intelligence (AI) model GPT-4 released by OpenAI can further strengthen Microsoft’s competitiveness in AI and to seize the search engines’ market share from Google. Microsoft as a leading technology company is expected to benefit from the development of artificial intelligence. It is recommended to buy at US$280.0, target at US$315.0, and stop loss at US$265.0.

S&P500 :

Source: Bloomberg

Key events:

| Key events | |

|---|---|

|

4/13 |

Initial and continuing jobless claims |

|

4/14 |

Industrial production, Consumer Sentiment, UNITEDHEALTH(UNH) results, JP MORGAN (JPM) results, WELLS FARGO (WFC) results, BLACKROCK (BLK) results, CITIGROUP (C) results |

Sector 1 week performance :

| (%) | |

|---|---|

|

Energy |

3.51% |

|

Utilities |

2.60% |

|

Basic Materials |

-0.86% |

|

Real Estate |

-0.57% |

|

Healthcare |

2.53% |

|

Consumer Defensive |

0.61% |

|

Industrials |

-2.56% |

|

Communication Services |

1.70% |

|

Technology |

-1.77% |

|

Financial |

-0.24% |

|

Consumer Cyclical |

-2.73% |

Source: Bloomberg, finviz

Stock: Cisco (CSCO.US)

Source: Bloomberg, finviz

Stock: Microsoft (MSFT.US)

Source: Bloomberg, finviz

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓