The tension between China and the United States has increased. After the United States shot down a Chinese balloon, U.S. blacklisted 6 Chinese entities involved. U.S January PPI rose 0.7% MoM /6% YoY higher than the expected increase of 5.4%. Coupled with the solid labour market, market expects that the Fed to raise interest rates by 0.5% in March. The investment sentiment has been affected. In addition, the exchange rate of the Hong Kong dollar also weakened, and the one-month interbank rate once dropped to ~ 2.12%, which may reflect the weakening demand for the Hong Kong dollar, which is echoed in the unfavorable investment market.

Link REIT (823) announced 1-for-5 rights issue with a 30% discount, which dragged down the share price performance of Hong Kong properties. However, equity financing can help to reduce debt and provide more resources for further development, which will benefit shareholders in the long run. In addition, the local real estate market has continued to pick up, both the transaction volume and property prices have rebounded. The correction of real estate stocks brought better entry points. Among the developers, Kerry Properties (683) will launch nearly 1,800 units in 23E and focus on Luxury residential projects, while it has higher than peers’ income from investment properties (>50%). The GFA of investment properties is expected to increase by more than 100% in the next 5 years. We expect the stock price to outperform peers. Hang Seng (11), HSBC (5), Baidu (9888), Alibaba (9988) and Hong Kong Stock Exchange (388) will announce their results during the week of 2/20-2/24, which are expected to become the focus of the market. The technical trend was weak with the Hang Seng Index staying below the 10-days and 20-days SMA. In addition, as some brokers may suspend account opening for new Chinese customers, which may affect the investment sentiment and capital flow. We expect the Hong Kong market to come under pressure in the near term and to trade between 20,000 and 21,500. 兩會 (NPC, CPPCC) which will be held in 4-5 March will be another focus of the market.

Chinese household savings increased by CNY 6.2tn in Jan, a record high for the same period in history. As consumer sentiment and the economy continues to recover, we believe part of the savings can be turned into consumption and benefit the retail sectors.

Vinda (3331): The company is mainly engaged in the production of household paper and personal care products. In 2022, the company’s revenue was HK$19.42 bn +4% YoY, in which household paper (accounting ~83% of total revenue) +3.9% to HK$16.1bn and personal care products (accounting ~17% of total revenue) +4.4% YoY to HK$3.31 billion. Net profit in 2022 was HK$706 mn, -57% YoY. For 4Q22, revenue was HK$5.363 bn, -2% YoY, and Net profit dropped 95% YoY to HK$19mn.

The drop in net profit is mainly due to the increase in raw material prices (including pulp, packaging and energy). As pulp cost accounted for about 50%-70% of the company’s overall cost of household paper, the price movement of pulp cost has material impact on the profitability. Looking forward, mgmt believes the cost of raw materials to decline in 2023 while the market expects pulp prices to have double digit decline in 23E, which can improve the performance of Vinda in 23E. With the relaxation of Covid measures and normalization of economic activities, we believe the company’s result to have already bottomed. It is recommended to buy at$ 21.3, target at $24, stop loss at $20. Risks: Weaker-than-expected recovery in consumer sentiment.

China Modern Dairy Holdings (1117) is mainly engaged in production and sales of milk, in which 80% of sales is to MENGNIU(2319). During 1H22, the company’s revenue was CNY 5.63 bn, +77.1% YoY, and the net profit was CNY 530 mn, +5% YoY. During the period, the average production cost of raw milk increased by 5.1% YoY to CNY 2.9/kg, and further increased to CNY 3.1/kg in December. However, mgmt aims to keep the gross profit margin above 30% by (1) increasing milk production and (2) fixing the corn cost (accounting ~40% of feed cost/ ~30% of COGS).

Market expects fresh milk production in China to have 3% YoY growth for 2023E, while management also expects volume to increase gradually by increasing the herd size to 500K heads by 25E (1H22~380K) and the annualized unit yield per cow to go up from ~12 tons to 13 tons. For 23E, management expects ASP to remain flat (1H22 was CNY4.28/kg) while volume to grow at high single digit and up to ~2.5mn tons per year. With (1) full re-opening of China, (2) focus on cost control, (3) stable volume growth, we believe CMD is fundamentally well positioned to benefit once the consumer sentiment rebound in China. It is recommended to buy at$1.12, target at $1.3, stop loss at $1.05. Risks: ASP in short term face downward pressure.

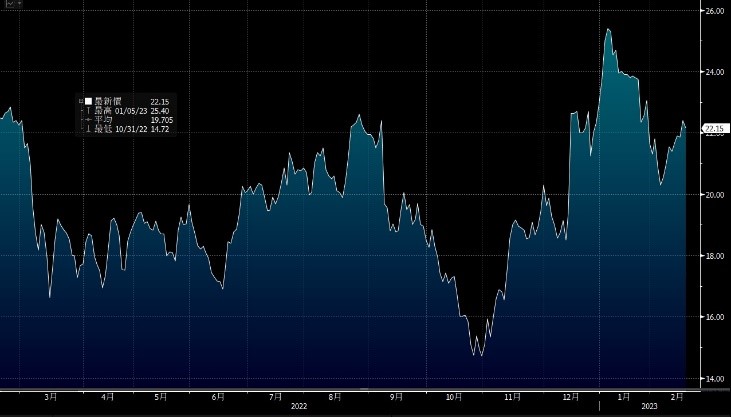

HSI:

Source:Bloomberg

Key events for the week:

LINK REITs (823 HK) 1-for-5 rights issue with 30% discount |

Standard Chartered (2888 HK) EBT +28% YoY to US$4.286 bn |

BEA (23 HK) net profit-17.3% YoY to HK$4.36 bn |

China’s Jan air passenger numbers +34.8% YoY |

New home price in tier cities +2.1%YoY in Jan |

China Jan production/sales volume of commercial vehicles -24%/-38% YoY. |

| Key events for next week: | |

|---|---|

|

02/21 |

Hang Seng Bank (11 HK) results, HSBC (5 HK) results, Sino (83 HK) results |

|

02/22 |

Baidu (9888 HK) results |

|

02/23 |

Alibaba (9988 HK) results, Hong Kong Stock Exchange (388 HK) results, Sun Hung Kai Properties (16 HK) results |

Sector performance:

| Weekly performance(%) | |

|---|---|

|

Utilities |

-1.7% |

|

Real estate |

-3.3% |

|

Industrial |

-3.2% |

|

IT industry |

-2.8% |

|

Financial |

-1.4% |

|

Energy |

-0.2% |

|

Raw material |

-1.9% |

|

Medical and health care |

-4.3% |

|

Telecommunications |

0.2% |

|

Consumer discretionary |

-2.3% |

|

Consumer staples |

0.0% |

Source:Bloomberg

Stock pick: Vinda (3331)

Stock pick: China Modern Dairy Holdings (1117)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓