The U.S. ISM Manufacturing Index for March was 50.3, significantly better than the expectation of 48.3, and the previous value in February of 47.8, which marked the first time since September 2022 that it returned to the expansion territory. The new orders index was 51.4, re-entering the expansion territory, compared to the expectations of 49.8 and the previous value in February of 49.2. The new export orders remained unchanged from February, at 51.6. The production index was 54.6, the highest since June 2022, with a significant MoM increase of 6.2 points, the biggest growth since mid-2020. The prices index was 55.8, the highest level since July 2022, compared to the expectations of 52.9 and the previous value in February of 52.5. The higher costs of materials and other inputs indicated that inflation pressures remained robust.

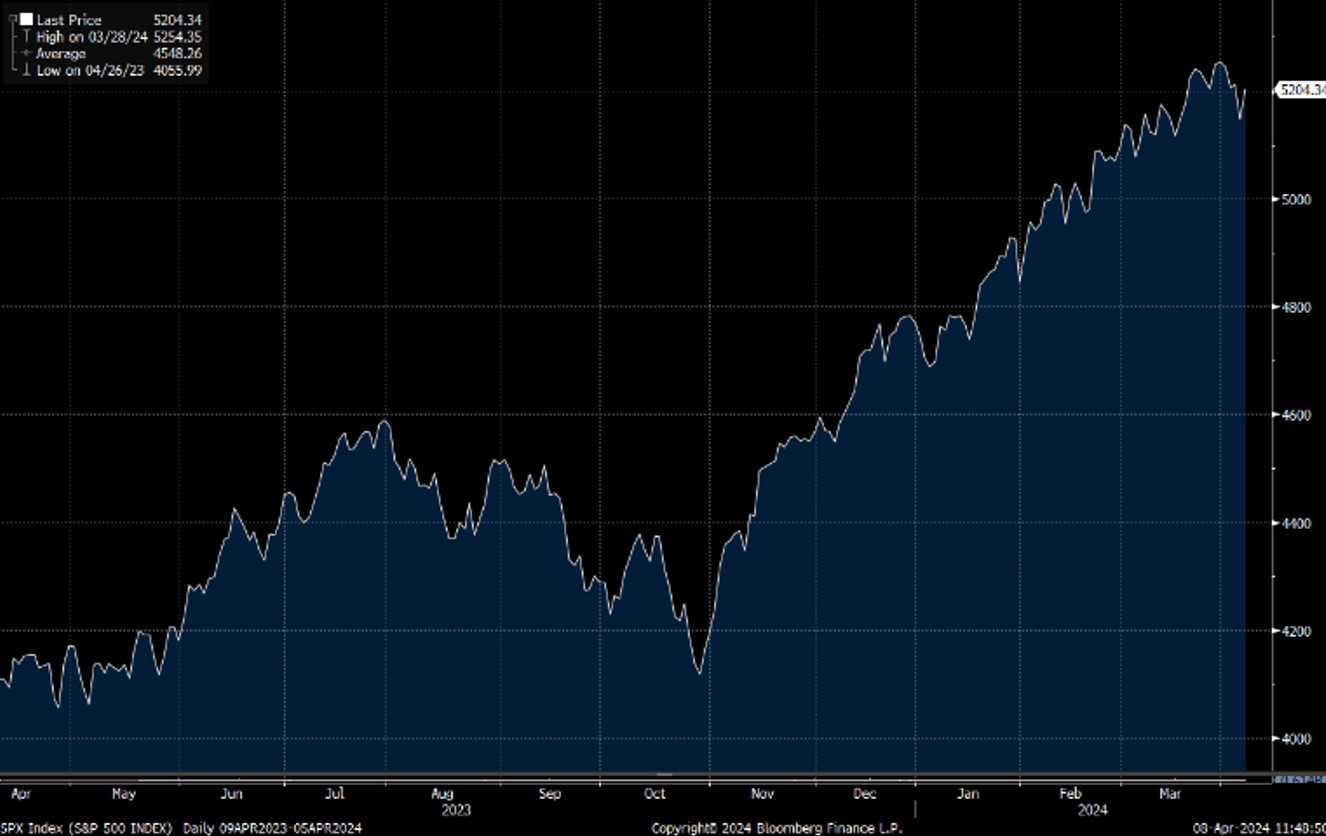

The employment index was 47.4, compared to the previous value in February of 45.9. Although the employment index was still in contraction territory in March, the contraction slowed compared to February. The inventory index was 48.2, an increase of 2.9 points from 45.3 in February. The March customer inventory index was 44, a decrease of 1.8 points from 45.8 in February, which indicated that the contraction of factory inventories in March was slower than in February, while the rate of contraction for customer inventories was faster. In terms of U.S. stock market, due to the hawkish comments from Federal Reserve officials that caused market concerns, the S&P index continued to decline last week. The S&P 500 Index is expected to fluctuate between 5,000-5,400 points in the short term.

In terms of industry, the pharmaceuticals industry has a stable growth rate and great market space in the medium to long term. Investors could pay attention to its earnings performance.

GSK(GSK.US) Total sales in 2023 amounted to £30.3 billion, up 5% YoY. In terms of segment, Vaccines sales was up 25% YoY to £9.9 billion. Specialty Medicines sales dropped 8% YoY to £10 billion, with HIV up 13% and Respiratory up 18% YoY. General Medicines sales increased by 5% to £10 billion. Total operating profit and net profit for 2023 reflects strong growth. Operating profit stood at £6.7 billion, up 10% YoY with OPM of 22%, while net profit increased by 14% YoY to £5.3billion, with NPM of 17.5%.

The pipeline progress remained strong, with 4 major product approvals, including Arexvy RSV vaccine, Apretude for HIV prevention, Ojjaara for myelofibrosis and Jemperli in 1L endometrial cancer. The Mgt maintained optimistic about FY24’s performance and expected turnover growth in FY24 of between 5% to 7% and adjusted operating profit growth of between 7% to 10%. It is recommended to buy at US$40.0, target at US$46.50, and stop loss at US$38.30.

AstraZeneca(AZN.US)Total Revenue in FY23 reached US$45.85 billion, up 6% YoY. Excluding COVID-19 medicines, total Revenue increased by 15% YoY and Product Sales increased by 14%. In terms of therapy type, Oncology revenue increased by 23% YoY to US$5.0 billion, showing strong performance across all key medicines and regions. CVRM revenue amounted to US$2.7 billion, up 18% YoY, on back of Farxiga up 36%, Lokelma up 38% and roxadustat up 27%. R&I revenue was up 13% YoY to US$1.7 billion.

The profitability of AstraZeneca continued to improve. Gross profit increased by 17% YoY to US$37.5 billion, with GPM of 82%, up 10ppts mainly due to positive effects from product mix. Net profit stood at US$6.0 billion, up 81% YoY, with NPM up 6ppts YoY to 13%. Final dividend declared at US$1.97 per share, making a total dividend declared for FY 2023 of US$2.90 per share, with a payout ratio of 75%. It is recommended to buy at US$65.50, target at US$76.00, and stop loss at US$62.50.

Source: Bloomberg

Key events

| Key events | |

|---|---|

|

04/10 |

Delta Air Lines (DAL.US) results release |

|

04/11 |

Constellation Brand (STZ.US) results release, Fastenal (FAST.US) results release |

|

04/12 |

JPMorgan Chase (JPM.US) results release, Wells Fargo (WFC.US) results release, Blackrock (BLK.US) results release, Citi (C.US) results release |

| Overall performance | |

|---|---|

|

Energy |

3.61% |

|

Utilities |

-1.88% |

|

Basic Materials |

0.51% |

|

Real Estate |

-2.92% |

|

Healthcare |

-2.84% |

|

Consumer Defensive |

-2.50% |

|

Industrials |

-0.33% |

|

Communication Services |

1.66% |

|

Technology |

-0.84% |

|

Financial |

-1.20% |

|

Consumer Cyclical |

-2.12% |

Stock: GSK(GSK.US)

Source: Bloomberg

Stock: AstraZeneca(AZN.US)

Source: Bloomberg

Analyst: CHAN Ka Kin (CE Number BHS185)

Disclosure of Interest

Neither the analyst(s) preparing this report nor his associate has any financial interest in; or serves as an officer of the listed corporation covered in this report. The remuneration of the analyst(s) is not directly or indirectly related in any way to the particular opinions or views expressed in this report.