According to the National Bureau of Statistics, China’s April economic data appeared to be stable. Despite the effect of holidays and high base from the prior year, overall improvements were seen in key indicators such as industrial output, exports, employment, and prices. New growth drivers maintained their strong pace while the underlying economy is gaining momentum for further recovery. However, it should be noted that the external environment is adding uncertainties and posing many challenges and difficulties to sustain the current recovery path.

In April, industrial output grew 6.7% YoY, a further 2.2 ppts gain compared to the previous month. The total retail sales of consumer goods rose 2.4% YoY, down from the previous 3.1%. From January to April, FAI advanced by 4.2% YoY, down from 4.5% in the prior period. The urban unemployment rate in April stood at 5%, down from the previous 5.2%.

During the initial four months of the year, a total of RMB3.09tn has been deployed into real estate development, representing a YoY drop of 9.8%. Among them, residential investment totaled RMB2.34tn, down 10.5% YoY. In addition, selling price of properties in 70 large and medium-sized cities are generally continuing their downtrend.

For the stock market, the HSI is expected to challenge the 20k mark fueled by the recent PBOC’s stimulus plan to the property market which include the lifting of interest rate floor and relaxing mortgage down payment on first and second home. However, given the significant jump in recent days, it is anticipated that the Index may likely consolidate between 19k to 20k in the near term.

In terms of sector pick, the recent capital inflow and positive policies to the Chinese’s property market could stimulate the consumer market.

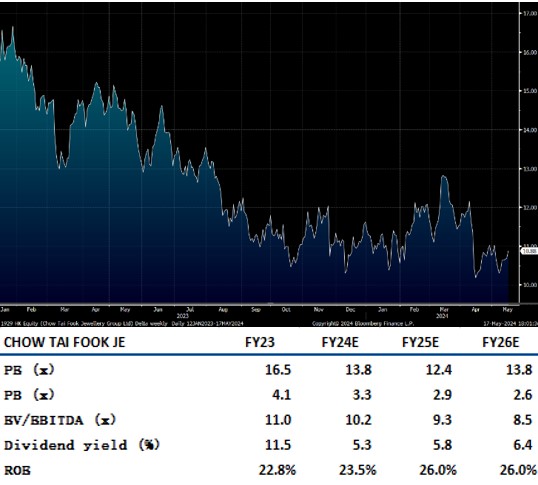

Chow Tai Fook Jewellery (1929.HK) is expected to announce its FY3/24 results in early June. Leveraging on strong gold prices and effective cost control, both revenue and profit margin are expected to improve. In 1Q 2024, CTF record a 12.4% YoY gain in total sales revenue where both Hong Kong/Macau and Mainland markets saw similar trend. The sales growth in HK/Macau was mainly from the increased sales of gold products and a 4.5% SSSG. Meanwhile, the mainland market was experiencing incremental performance from new shops and increased online sales.

The company’s mainland business is mainly conducted via franchising, allowing higher flexibility in the expansion and reduction of stores. With the current network size of over 7,500 outlets in China, CTF can no longer rely on opening new stores for growth. Instead, they should focus on evolving into a more efficient operating model to stabilize profit margins. Overall, CTF is a highly recognized brand and should benefit during consumption recovery. It is recommended to buy

at HK$10.55 with a target of HK$12.30 and stop loss at HK$10.10.

China Tourism-H (1880) first quarter core profit beat expectations and reached RMB2.3bn. Turnover down 9% to RMB1.88bn but still far better than Hainan’s offshore duty-free shops which saw a 20 to 30% YoY decline. The stronger performance reflects an improvement in sales at the airport duty frees. GPM stood at 33.3%, up 4.3% YoY.

The company spent the previous year selling down its inventories to avoid further price cuts and stabilizing its profit margins. In addition, adopting new prices and improving product mix are likely to drive topline recovery. The positive effects of the newly imposed rental terms at Hainan airport will likely kick in this year. There was a survey indicating that inventory of cosmetics in Hainan has been cut by 1/3 which is inline with positive view that Estee Lauder and L’Oreal have on the Asian travel market. With more new in-town duty shops to be opened, the Mgt is positive about its growth. It is recommended to buy at HK$72.50, target at HK$84.50, and stop loss at HK$69.50.

HSI:

Source:Bloomberg

Key events for the week:

- Tencent (700.HK) 1Q adjusted profit up 54% YoY, beat expectations

- Alibaba (9988.HK) 1Q adjusted profit down 11% YoY and paying a total dividend of 20.75 US cents

- Samsonite (1910.HK) 1Q profit US$82.9mn, up 12% YoY

| Key events for next week: | |

|---|---|

|

05/20 |

PBOC 5-yr LPR |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

5.5% |

|

Real estate |

12.0% |

|

Industrial |

2.0% |

|

IT industry |

6.8% |

|

Financial |

7.0% |

|

Energy |

1.5% |

|

Raw material |

5.2% |

|

Medical and health care |

0.3% |

|

Telecommunications |

4.8% |

|

Consumer discretionary |

0.5% |

|

Consumer staples |

1.5% |

Source:Bloomberg

Stock pick: Chow Tai Fook Jewellery (1929.HK)

Source:Bloomberg

Stock pick: China Tourism-H (1880.HK)

Source:Bloomberg

Analyst: CHAN Ka Kin (CE Number BHS185)

Disclosure of Interest

Neither the analyst(s) preparing this report nor his associate has any financial interest in; or serves as an officer of the listed corporation covered in this report. The remuneration of the analyst(s) is not directly or indirectly related in any way to the particular opinions or views expressed in this report.