The US Bureau of Labor Statistics has announced that the PPI for final demand in April increased by 0.2% from the previous month, which is lower than the market’s expectation of 0.3%. The YoY increase in PPI fell from 2.7% in March to 2.3% in April, which is the lowest since January 2021. The increase in the PPI for final demand in April was mainly due to an 8.4% increase in gasoline prices. The US CPI fell by 0.1pcts YoY to 4.9% in April, which is slightly lower than the market’s expectation. The core CPI, which excludes energy and food prices, also fell slightly by 0.1pcts YoY to 5.5% in April, which is at the lowest level since the end of 2021. The latest inflation data further validates the market’s expectation that the Federal Reserve will suspend interest rate hikes next month.

The US Bureau of Labor Statistics has announced that the non-farm payroll employment in April increased by 253,000, which is higher than the market’s expectation of 180,000. The unemployment rate in the US fell by 0.1pcts to 3.4% in April, which is a new low since 1969. The average hourly wage increased by 0.5% MoM, which is higher than the expected and previous values of 0.3%, and the YoY increase was 4.4%, which is higher than the expected and previous values of 4.2%. The US core PPI in April increased by 0.2% MoM, and the YoY increase fell from 3.7% in March to 3.4%, which is at the lowest level since March 2021. As of the week ending May 6th, the number of initial claims for unemployment benefits was 264,000, higher than the expected 245,000. This is the highest number of applicants since October 2021, further proving that the labor market is gradually cooling down. Looking ahead, with the Federal Reserve’s interest rate hikes and tightening credit conditions continuing to put pressure on the economy, more layoffs look imminent. We expect that there is a greater chance of short-term fluctuations in the US stock market, and the S&P 500 index is expected to fluctuate between 4,000 and 4,300 points.

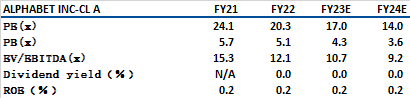

Alphabet Inc. (GOOGL.US) has released its 1Q23 financial report, with revenue of USUS$69.79 bn, up 3% YoY, which is higher than the expected US$68.9 bn. The net profit was US$15.05 bn, with EPS of US$1.17, up 4.9% YoY, which is also higher than the expected US$1.07. The company’s cloud business revenue increased by 28.1% to US$7.45 bn, and it achieved profitability for the first time, with an operating profit of US$191 mn.

Google Cloud’s contract volume in the past three years has increased by 300%, including 60% of the world’s top 1,000 companies. The company’s AI-as-a-service business has also benefited from the development of the industry. Although the company’s advertising business performed better than expected, the overall online advertising spending is not expected to decline. Google continues to repurchase shares, demonstrating its financial strength and confidence in future developments. In terms of AI, Google has stated that it will focus on search and productivity, promote the merger of Google Brain and Deep Mind, and develop its AI chip TPU, which has been used in Google Cloud since 2015 and has now been developed to the fourth generation. It is currently used to train large models such as PaLM with 540 bn parameters. It is recommended to buy at US$114.0, target at US$132.8, and stop loss of US$109.3.

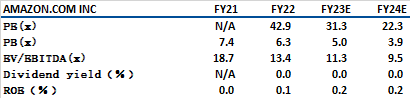

Amazon (AMZN.US) has released its Q1 FY23 earnings report, with net sales of US$127.36 bn, up 9% YoY from US$116.44 bn in the same period last year. Excluding the impact of exchange rate fluctuations, the net sales increased by 11% YoY. The net profit was US$3.17 bn, compared to a net loss of US$3.84 bn in the same period last year, and the diluted EPS were US$0.31, compared to a diluted EPS of US$-0.38 in the same period last year. Amazon’s Q1 product net sales were US$56.98 bn, up from US$56.46 bn in the same period last year, and service net sales were US$70.38 bn, up from US$60.0 bn in the same period last year.

AWS (Amazon Web Services) is the company’s main source of profit, and the company’s Q1 highlight has been AWS exceeding expectations. In addition, the company’s advertising business also performed better than expected. Although the company invested less in AI than Google, Microsoft, and META, it also launched AI training chips integrated into AWS. The mgt stated that the company will put more resources into AI business through AWS, iterate the existing large models of ALEXA. It will continue to increase investment in AI in advertising business while reducing logistics expenses. It is recommended to buy at US$106.9, target at US$124.6, and stop loss at US$102.5.

S&P500:

Source: Bloomberg

Key events :

|

5/15 |

WALMART INC. (WMT) results |

|

5/16 |

HOME DEPOT, INC. (HD) results |

|

5/17 |

CISCO SYSTEMS, INC. (CSCO) results |

|

5/18 |

Initial Claims (SA)、Insured Unemployment (SA) |

|

5/19 |

DEERE & COMPANY (DE) results |

Sector 1 week performance:

| (%) | |

|---|---|

|

Energy |

-1.48% |

|

Utilities |

0.15% |

|

Basic Materials |

-2.85% |

|

Real Estate |

-1.04% |

|

Healthcare |

0.87% |

|

Consumer Defensive |

-0.55% |

|

Industrials |

-0.79% |

|

Communication Services |

4.84% |

|

Technology |

-0.15% |

|

Financial |

-1.08% |

|

Consumer Cyclical |

0.33% |

Source: Bloomberg, finviz

Stock: Google (GOOGL.US)

Source:Bloomberg

Stock: Amazon (AMZN.US)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓