The National Bureau of Statistics announced that the total retail sales of consumer goods in March was CNY3.79 tn, +10.6% YoY, which was higher than market expectations of 7.5%. The retail sales of consumer goods other than automobiles were CNY3.36 tn, +10.5% YoY. The total retail sales of social consumer goods in the first quarter reached CNY11.49 tn, +5.8% YoY, which was also higher than the expected increase of 3.7%. Among that, the retail sales of consumer goods other than automobiles were CNY10.41 tn, +6.8% YoY. Household commodity consumption is still at the early stage of recovery, and it is expected to pick up further in the future. With the improvement of business operations and financial expenditures, consumption may maintain a healthy trend and continue to support retail sales. Since consumer confidence has gradually recovered, the economic recovery driven by the service industry may also stimulate employment.

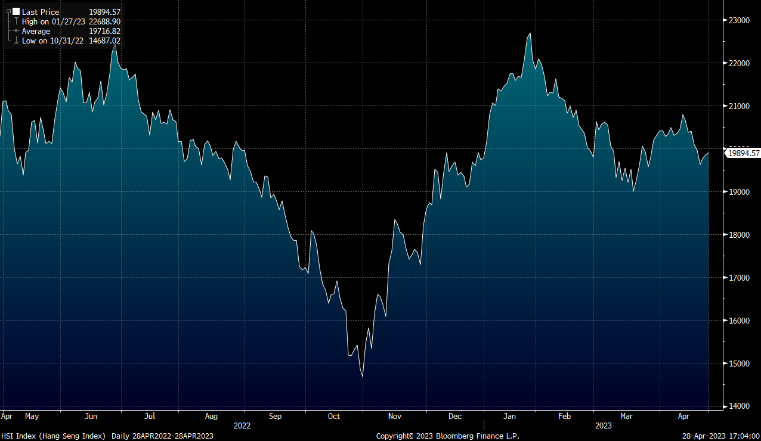

The Rating and Valuation Department announced that the private residential price index in March rose 1.4% MoM, up for three consecutive months, with a cumulative increase of about 5% in the first quarter; the “Midland Property Price Index” rose 5.9% in 1Q23, breaking the two-quarter decline in the third and fourth quarters of last year. With the significant rebound in property prices in the first quarter, the room for property owners to negotiate prices has narrowed. As recent second-hand transactions have slowed, it may lead to some property owners to quick sell at a discount. However, looking forward into the second quarter, the economy is gradually improving. The upward trend in property prices should continue in the second quarter, but the growth rate is expected to slow. The Midland Property Price Index has increased slightly by 0.3%, which is relatively slow, and it has gone up by 6.3% so far this year. As Hong Kong’s economy is gradually returning to normal, property prices are expected to rebound from low levels this year. Regarding the Hong Kong market, as it lacks upward momentum, we expect HSI to trade between 19,300-20,500 points.

In terms of industry, although the domestic economic data in the first quarter was better than expected, the market is more forward-looking to look at the sustainability of the current trend. Investors should pay attention to consumer stocks with expected better performance.

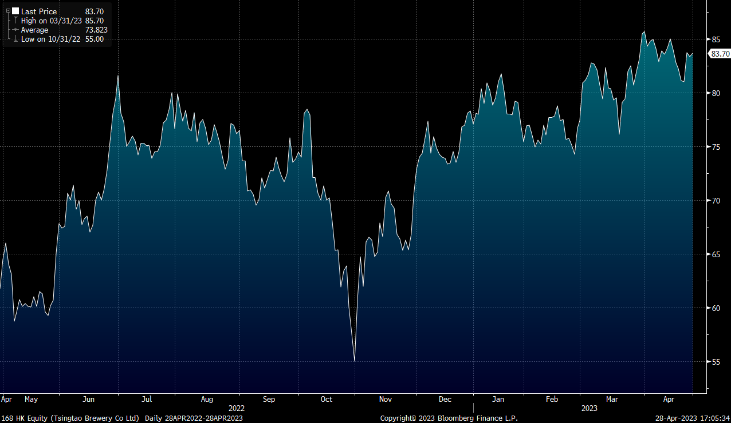

Tsingtao Brewery (168.HK) announced its operating performance in the first quarter of 2023. In 1Q23, the company recorded operating income of CNY10.71 bn, +16.3% YoY. The company achieved product sales of CNY2.363 mn kiloliters, a YoY increase of 11.0%. The net profit attributable to shareholders was CNY1.45 bn, +28.9% YoY; the company’s net profit not excluding non-recurring item was CNY1.35 bn, +32.1% YoY.

In 1Q23, the company’s product sales reached 2.363 mn kiloliters, +11.0% YoY. The main brand Tsingtao Beer achieved sales of 1.401 mn kiloliters, +7.5% YoY. The sales volume of medium and high-end products reached 984,000 kiloliters, +11.6% YoY. Looking ahead, the company will continue to implement the “1 (Tsingtao Beer) + 1 (Laoshan Beer)” brand strategy, to promote the brands vigorously, and to enhance its competitive advantages in the mid-to-high-end market. Relying on consumer personal experience marketing methods such as “Tsingtao Beer Time Coast Craft Beer Garden” and “TSINGTAO1903 Tsingtao Beer Bar”, it continues to meet the multi-level needs of consumers. It is recommended to buy at HK$81.2, target at HK$94.6, and stop loss at HK$78.7.

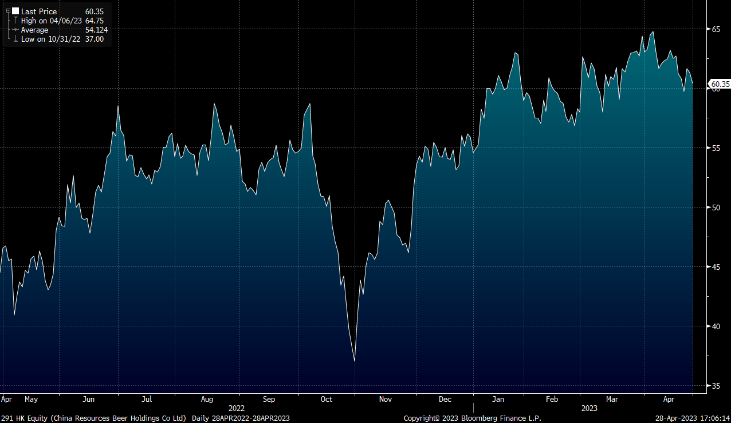

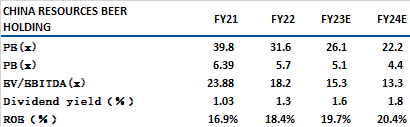

China Resources Beer (291.HK) has a total operating income of 35.263 bn yuan in FY22, +5.62% YoY; the net profit was CNY4.52 bn, +26.9% YoY, and the performance was in line with expectations. In terms of gross profit margin, affected by the rising costs of raw materials and packaging, the company’s production costs were under pressure. The cost per ton increased by 6.5% YoY to CNY1956 per kiloliter, and the gross profit margin fell by 0.7pct to 38.5%.

Looking forward to 23E, the company will continue to increase its high-end brand building. While building a large customer platform, it will also promote the construction of the “Second Batch of Excellence”. It has signed contracts with customers in Fujian, Zhejiang and other regions. In 23E, the sales growth is expected to increase more than 20%, and the product is expected to continue to be upgraded, driving the company’s volume and ASP. In addition, the company’s FY23 cost pressure is expected to ease. The company’s lean sales expenses together with the optimization of other management expenditures, total costs are expected to be further reduced, and the company is expected to maintain a double-digit growth. It is recommended to buy at HK$61.2, look up at HK$71.3, and stop loss at HK$59.3.

HSI:

Source:Bloomberg

Key events for the week:

BYD (1211.HK) recorded net profit of CNY4.13 bn in 1Q23 |

CITIC Limited (267.HK) net profit rose 10.4% YoY to CNY 14.98 bn in 1Q23 |

Prudential (2378.HK) profit up 30% to US$743m in 1Q23 |

Sinopharm (1099.HK) recorded revenue CNY1.59 bn in1Q23, +11.4% YoY |

| Key events for next week: | |

|---|---|

|

05/02 |

HSBC PMI |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

1.3% |

|

Real estate |

-0.3% |

|

Industrial |

-2.8% |

|

IT industry |

-3.0% |

|

Financial |

0.7% |

|

Energy |

2.4% |

|

Raw material |

-3.2% |

|

Medical and health care |

-1.8% |

|

Telecommunications |

0.6% |

|

Consumer discretionary |

-0.6% |

|

Consumer staples |

-0.9% |

Source:Bloomberg

Stock pick: Tsingtao Brewery (168HK)

Stock pick: China Resources Beer (291 HK)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓