The Mortgage Bankers Association (MBA) announced on March 29 that after seasonal adjustment, the Market Composite Index (Market Composite Index), which measures the number of mortgage applications for the week ended March 24, rose 2.9% WoW. According to MBA statistics, the Refinance Index increased 5% WoW and reached a new high since Sept 22 and dropped 61% YoY. As of the week ended March 24, the 30-year mortgage rate declined to 6.45%, marking a three-week consecutive decline. Although it is 1.65% higher than last year, recent data has been improving, and the market believes that the US real estate market can continue to improve.

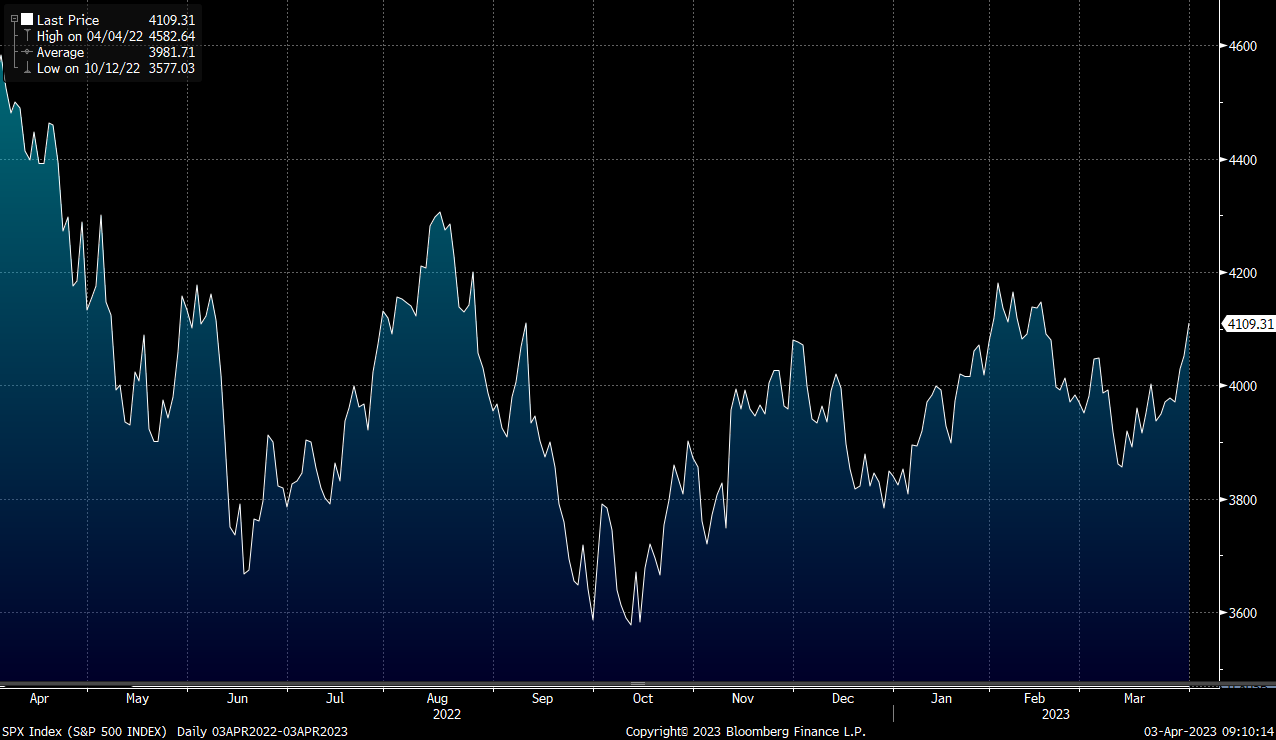

According to data released by the US Department of Labor, jobless claims for the week ended March 25 totaled 198,000, up 7,000 from the previous period and a bit higher than the estimate of 195,000. Continuing jobless claims was 1.689 mn, which was below the estimate of 1.6935 mn. The market expects initial jobless claims to eventually reflect layoffs in the technology, financial and media industries, and the banking crisis could also affect initial jobless claims. From the perspective of recession risk, higher unemployment rate, and the degree of credit tightening, the uncertainties in the investment market are increasing. We expect S&P 500 to trade between 3,800 and 4,500 points.

In terms of industry, the market expects limited room for the US to raise interest rates. Investors can focus on technology stocks with better performance and growth potential.

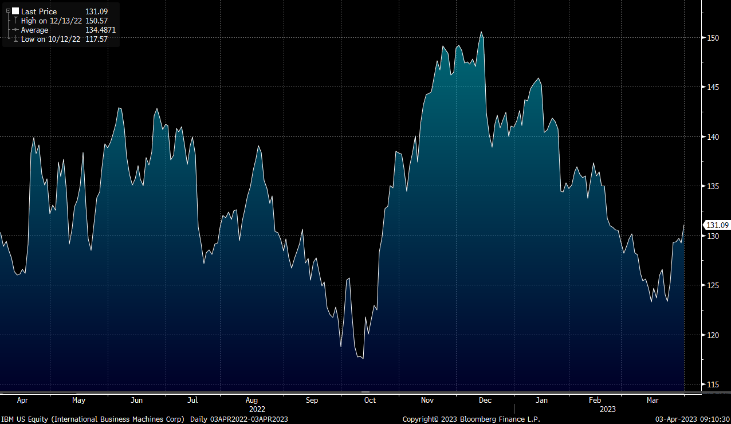

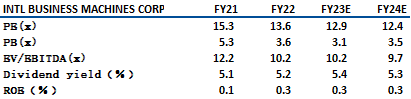

International Business Machines Corporation (IBM.US): The total revenue in the fourth quarter was US$16.7 bn, +6% YoY at constant exchange rates. For FY22, total company revenue was US$60.5 bn, +12% in constant currency. The revenue of IBM’s software business unit (including hybrid platform, solution and transaction processing business) in the fourth quarter was US$7.288 bn, +8.0% YoY excluding the impact of exchange rate changes.

Management expects full-year 2023 revenue to growth at between 1%-9% (excluding the impact of currency movements). More than 40,000 enterprise customers are using IBM’s AI product IBM (Watson), which can help enterprises solve all aspects of core business problems. Given that IBM is the global leader in enterprise-level AI technology and applications, it is recommended to buy at US$127.0, target at US$143.0, and stop losses at US$119.5.

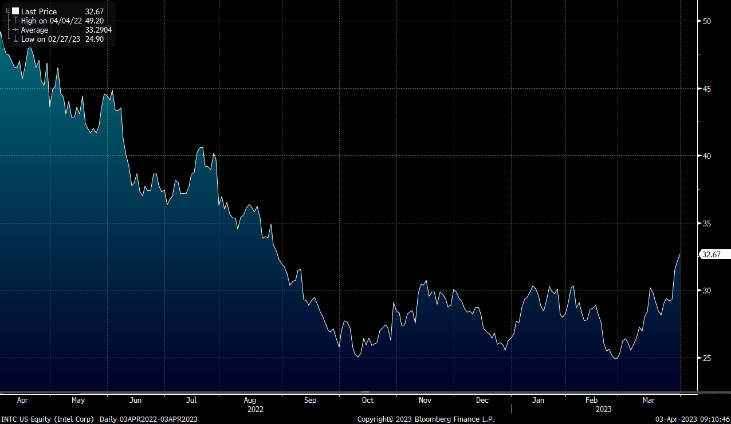

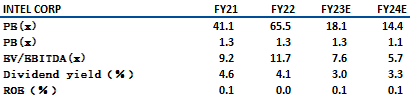

Intel (INTC.US) has released its fourth quarter and full year results for 2022. Affected by the continual sluggish demand in the global PC market in 4Q22, the company’s Q4 revenue was US$14.042 bn, -31.6% YoY; the gross profit margin was 39.17%, -14.46pct YoY; A quarterly loss of $664 mn. For the full year of 2022, the company’s revenue was US$63.05 bn, -20.21% YoY; the company’s gross profit margin was 42.61%, -12.84pct. However, the company’s emerging business maintained a relatively high growth. The FY22 revenue of the autonomous driving subsidiary Mobileeye increased by 35% YoY; the FY22 revenue of the foundry business was US$895 mn, +14% YoY.

In terms of business lines, Intel’s two main businesses were affected by demand and intensified competition in the downstream market. The revenue of the client computing sector in 2022 fell by 23% YoY, and the revenue of the data center & AI business down 15% YoY. However, the company’s emerging business is still in the growth stage, the segment is expected to have accelerated growth in the future. In 2023, digital construction will be steadily promoted in many fields, bringing new momentum to the development of the industrial chain, which is likely to boost the market demand for various semiconductor hardware and accelerate the construction of big data centers. It is recommended to buy at US$31.8, target at US$36.0, and stop loss at US$30.0.

S&P500 :

Source: Bloomberg

Key events :

| Key events: | |

|---|---|

|

04/03 |

PMI |

|

04/06 |

Initial and continuing jobless claims |

Sector 1 week performance:

| (%) | |

|---|---|

|

Energy |

6.1% |

|

Utilities |

3.7% |

|

Basic Materials |

5.2% |

|

Real Estate |

5.1% |

|

Healthcare |

2.3% |

|

Consumer Defensive |

2.7% |

|

Industrials |

4.5% |

|

Communication Services |

1.0% |

|

Technology |

3.8% |

|

Financial |

3.9% |

|

Consumer Cyclical |

6.0% |

Source: Bloomberg, finviz

Stock: International Business Machines Corporation (IBM.US)

Source: Bloomberg

Stock: Intel (INTC.US)

Source: Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓