Although China has lowered the RRR for financial institutions by 0.25% to around 7.6%, the market expects that RRR cut can potentially release ~CNY500bn of liquidity. As the magnitude of the cut is quite restrained, market does not expect much looser monetary policy in anytime soon, the cut had not brought a significant positive impact to the market. Fed raised interest rates by 0.25% as expected and signaled at least one more hike this year. According to Fed ‘dot plot’, the interest rate will peak at 5.1% in 2023. Although US Treasury Secretary Yellen said US is prepared to further support banks’ depositors if needed, the Fed had lowered its US economic growth forecast for the next two years. We expect Hong Kong stocks to remain volatile in the near term.

UBS takes over Credit Suisse for CHF$3.0 billion, however, Credit Suisse also said CHF16 bn of its Additional Tier 1 debt will be written down to zero. Market concerns about the risk of CoCo bonds of financial institutions has dragged the Hang Seng Index below 19,000 at one point. Although we expect the investment market to remain volatile, we believe that there is limited downside for Hang Seng Index as the probability of a larger scale financial system failure to be low. The VHSI (Volatility Index) of the Hang Seng Index stays around 27, reflecting the market risk aversion has remained high. Technically, Hang Seng index is above 10-days and 250 days SMA but has yet to return to the 20,000 level, technical trend remains weak. Investors may focus on liquidity and confidence issue in the European and American financial industry after the results peak season. We expect Hang Seng index to trade between 19,000 -20,500 points.

The market expects limited upside for US interest rates, which has driven the performance of technology stocks. As artificial intelligence continues to be a market focus, semiconductor companies are also expected to benefit from its development, the related stocks are worth some attention.

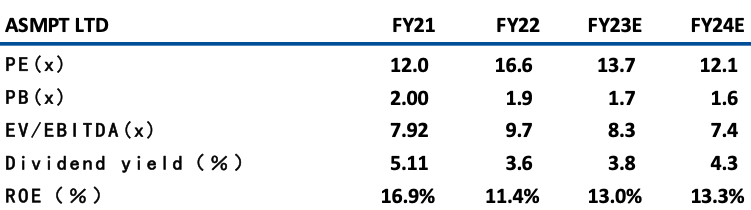

ASMPT (522 HK) is engaged in the design, manufacture and marketing of machines, tools and materials used in the semiconductor industry and surface mount technology placement machines. In 2022, the rev was HK$19.3bn, -11.8% YoY, in which semiconductor solution (accounting for 52% of total revenue) dropped 25.2% YoY to HK$10.1bn, and SMT solution (accounting for 48% of total revenue) increased 9.8% to HK$9.259 bn. The net profit was HK$2.62bn, -17.3% YoY.

Mgmt targets revenue in 1Q23 to be US$455mn to 525mn (-27.4% YoY and -11.4% QoQ at mid-point). However, mgmt aims bookings to grow 10%-20% QoQ in 1Q23. In the longer term, mgmt expects the Global Semiconductor Device Market to have CAGR of 8.2% 22-27E, the medium and long-term prospects of the company are still looking good. Although the industry is in a downward cycle in the short term, management is still optimistic about its advanced packaging and automotive business. It is expected that the advanced packaging and automotive business to have CAGR of 13% and 10% from 23 to 27E. In addition, the company is also expected to benefit from the development of ChatGPT, as its customers also include GPU, CPU and memory chips companies. It is recommended to buy at HK$73.0, target at HK$82.0, stop loss at HK$69.0. Risk: If the industry fails to recover as expected in 2H23, it may bring pressure onto the share price.

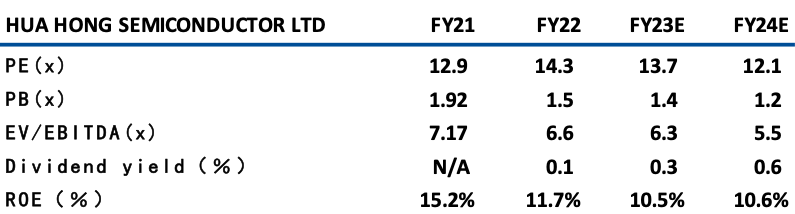

HUA HONG SEMI (1347 HK) is principally engaged in the manufacture and sale of semiconductor products. In 2022, the company’s revenue was US$2.475 bn, +51.8% YoY, the net profit for the period was US$450 mn. The overall gross profit increased by 86.8% to US$844 mn and the gross profit margin increased by 6.4% to 34.1%, mainly due to the increase in the ASP and the optimization of product mix. During the year, wafer shipments increased 22.8% to 4.09 mn pieces, and capacity utilization remained flat at 107.4%.

Mgmt expects 1Q23 revenue to be US$630mn (flat QoQ), while gross margin drop to 32%-24% from 38.2% in 4Q22. Although the industry is still in a down cycle, mgmt is confident that it can outperform its peers. At the same time, the company also reiterated the capacity expansion plan for the 12” fab. The 12”fab capacity is expected to expand from 65k wafer/month in late 2022 to 95k wafer/month in 2023E. Meanwhile, the construction of the second 12″ fab is to begin in 1H23 at the earliest, and the contribution could commence from 2H24 (total 12” wafer/month is expected to reach 125k in 25E). With the increase in production capacity and efficiency improvement, the company’s future revenue and gross profit are expected to improve. It is recommended to buy at HK$33.5, target at HK$38.0, stop loss at HK$32.0. Risks: Nearly 60% of the company’s revenue comes from consumer electronics products. The global recession may affect the company’s performance. |

HSI:

Source:Bloomberg

Key events for the week:

| China has lowered the RRR of financial institutions by 0.25% |

| CTF (1929 HK) SSS in HK/MO Grows 70.2% YoY in 2M23, dropped 11.8% YoY in China |

| Sunny (2382 HK) Net profit -51.7% YoY to CNY2.408bn |

| In Feb22, sales of China’s mobile game were CNY21.6bn, -2.76% MoM, or +2.03% YoY |

| Tencent (700 HK): Net profit in 22 was CNY188.2bn, -16% YoY |

| AAC TECHNOLOGIES(2018 HK): Net profit dropped 38% YoY to CNY820mn |

| CHINA RES BEER (00291 HK): 2022 Net profit down 5.3%YoY to CNY4.344bn |

| Key events for next week: | |

|---|---|

|

03/27 |

Profit of enterprise above designated size |

|

03/28 |

BYD (1211 HK) results, |

|

03/29 |

Country Garden Services (6098 HK) results, CR Land (1109 HK) results, PetroChina (857 HK) results, |

|

03/30 |

Country Garden (2007 HK) results, Haidilao (6862 HK) results |

|

03/31 |

PMI |

| 1 week performance(%) | |

|---|---|

|

Utilities |

-2.7% |

|

Real estate |

-0.76% |

|

Industrial |

1.0% |

|

IT industry |

7.5% |

|

Financial |

-0.1% |

|

Energy |

-2.1% |

|

Raw material |

-.2% |

|

Medical and health care |

-1.0% |

|

Telecommunications |

-4.1% |

|

Consumer discretionary |

2.9% |

|

Consumer staples |

0.9% |

Source:Bloomberg

Stock pick: ASMPT (522 HK)

Stock pick: HUA HONG SEM (1347 HK)

資料來源:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓