The National Bureau of Statistics announced that the manufacturing PMI in April was 50.4, 0.4 points down from March’s 50.8, maintaining the expansion. In terms of the size of enterprises, the PMI for large corporates was 50.3, a decrease of 0.8 points compared to the previous month. The PMI of small and medium-sized enterprises was 50.3 and 50.7 respectively, both above the threshold. Production continued to improve, but demand dropped significantly. The production index in April was 52.9, compared to the previous value of 52.2. The new orders index was down to 51.1 from 53.0 in March. The production and business activities expectation index dropped to 55.2 from 55.6 in March. The export and import components also showed a downward trend. The new export orders and import index were 50.6 and 48.1 respectively.

The non-manufacturing PMI for April was 51.2, a decrease of 1.8 points from the previous month. In terms of industries, the business activity index for the construction sector was 56.3, 0.1 points above the previous month, while the business activity index for the service industry was 50.3, a MoM increase of 2.1 points. For the respective businesses, railway transportation, road transportation, postal services, telecommunications, radio and television, and satellite transmission services were in the high expansion range of more than 55. However, the business activity indices for catering, capital market services, real estate were below the threshold. In terms of the Hong Kong stock market, as the return of foreign funds and the net purchase of southbound capital has driven the Hang Seng index to 18,000. The Hang Seng Index is expected to maintain upward momentum and fluctuate between 17,900 – 19,000 points.

In terms of industry, the fundamentals of the internet industry remains resilient, and the upward trend is expected to be clear. In addition, internet companies still have high growth potential. Investors can pay attention to it.

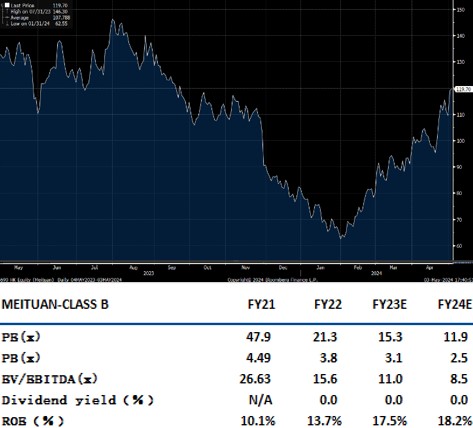

Meituan(3690.HK)’s revenues in FY23 increased by 25.8% to RMB276.7 billion. The net profit amounted to RMB13.9 billion, compared to the loss of RMB6.7 billion in FY22. In terms of segment, revenue from the Core local commerce segment increased by 28.7% YoY to RMB206.9 billion, thanks to the rapid recovery of local businesses. GTV of in-store, hotel and travel businesses increased by over 100% YoY in 2023. The YoY growths of Annual Transacting Users and Annual Active Merchants exceeded 30% and 60%, respectively. In addition, Meituan Instashopping posted another stellar growth with order volume increasing by over 40% YoY in 2023.

Revenues from the New initiatives segment increased by 18.0% YoY to RMB69.8 billion. The company steadily improved the operational efficiency through supply chain optimization and fulfillment cost reduction. Although New initiatives segment still recorded losses, operating loss narrowed from RMB28.4 billion in FY22 to RMB20.2 billion in FY23, with the operating margin up from negative 47.9% to negative 28.9%. It is recommended to buy at HK$116.0, target at HK$131.0, and stop loss at HK$108.0.

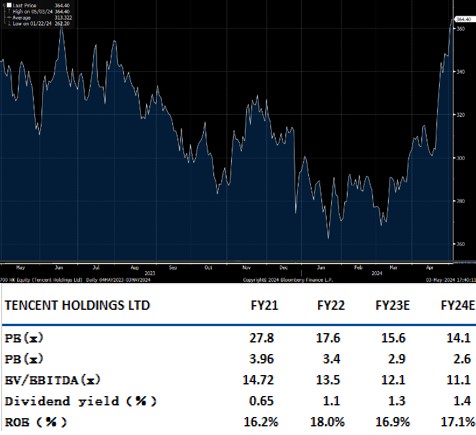

Tencent (700.HK) revenue in FY23 increased by 10% YoY to RMB 609 billion. Gross profit increased by 23% YoY to RMB 293.1 billion, with gross profit margin up 43% in FY22 to 48%. In terms of segment, revenues from Online Advertising increased by 23% YoY to RMB101.5 billion in FY23, driven by new inventories in Video Accounts and Weixin Search, plus the ongoing upgrade of the advertising platform, with notable step-ups in spending by consumer goods, Internet services and healthcare categories. Revenues from FinTech and Business Services rose by 15% YoY to RMB203.8 billion in FY23.

Revenues from VAS increased by 4% YoY to RMB298.4 billion in FY23. International Games revenues increased by 14% to RMB53.2 billion, benefitting from the robust performance of VALORANT and contributions from recently launched games Goddess of Victory: NIKKE and Triple Match 3D. Domestic Games revenues increased by 2% to RMB126.7 billion, on contributions from recently released VALORANT and Lost Ark. It is recommended to buy at HK$353.50, target at HK$399.50, and stop loss at HK$329.0.

HSI:

Source:Bloomberg

Key events for the week:

- MGM China (2282.HK) Q1 adjusted property EBITDA rose by 78%

- MGM China (2282.HK) Q1 adjusted property EBITDA rose by 78%

- Guangzhou Rural Commercial Bank (1551.HK) net profit in Q1 was approximately RMB1.47 billion, down approximately 26.1% YoY.

- Tsingtao Brewery (168.HK) net profit in Q1 amounted to RMB1.6 billion, up 10% YoY

| Key events for next week: | |

|---|---|

|

05/11 |

CPI:同比、PPI:同比 |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

0.1% |

|

Real estate |

9.6% |

|

Industrial |

5.3% |

|

IT industry |

8.8% |

|

Financial |

7.2% |

|

Energy |

2.0% |

|

Raw material |

3.3% |

|

Medical and health care |

6.9% |

|

Telecommunications |

-1.9% |

|

Consumer discretionary |

7.5% |

|

Consumer staples |

4.5% |

Source:Bloomberg

Stock pick: Meituan(3690.HK)

Source:Bloomberg

Stock pick: Tencent (700.HK)

Source:Bloomberg

Analyst: CHAN Ka Kin (CE Number BHS185)

Disclosure of Interest

Neither the analyst(s) preparing this report nor his associate has any financial interest in; or serves as an officer of the listed corporation covered in this report. The remuneration of the analyst(s) is not directly or indirectly related in any way to the particular opinions or views expressed in this report.