The Hong Kong Census and Statistics Department (C&SD) published the March Consumer Price Index (CPI). Overall CPI rose 2.0% YoY in March, down 0.1ppt from 2.1% in February. Excluding the impacts of one-off relief government measures, the Composite CPI rose by 1.0% YoY, compared to 1.2% in February. The respective increases in the CPI(A), CPI(B) and CPI(C) were 2.3%、1.9% and 1.7%. In terms of categories, alcohol and tobacco recorded the biggest jump, up 17.7% YoY, which was the main reason for the increase in March. Price of electricity, gas and water decreased by 8.7% YoY. Basic food prices also dropped by 0.5%. The YoY decline in durable goods prices stood at 1.5%. Clothing, dining out and takeaways, transportation, miscellaneous services and goods all increased.

The underlying consumer price inflation was modest in March. While prices of meals out and takeaway food continued to rise relatively quickly, prices of basic food edged down from a year earlier. Prices of energy-related items fell further. Price pressures on other major components remained broadly in check. Looking ahead, overall inflation should stay contained in the near term. Domestic costs may face some upward pressures as the Hong Kong economy continues to recover. External price pressures should remain on a broad downward trend. In terms of the Hong Kong stock market, Hong Kong stocks advanced for the fifth straight day, propelling the benchmark index to its highest close in five months, as investors bet that corporate earnings recovery will drive valuations with a host of company results due to be unveiled this month. The Hang Seng Index is expected to maintain its momentum and fluctuate between 17,100-18,200 points.

In terms of industry, due to the steady rebound of international oil prices, oil stocks have become the targets of stock market funds. The gains of oil stocks outperformed the market. Investors can pay attention to related companies.

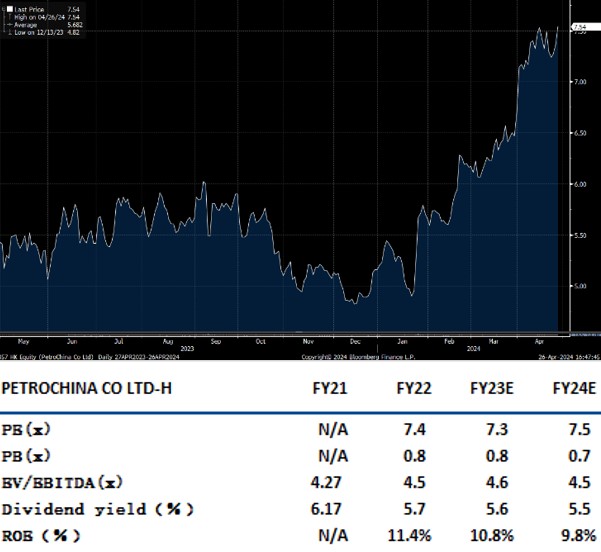

PetroChina(857.HK) achieved a revenue of RMB3,011 billion in FY23, representing a YoY decrease of 7.0%, mainly due to the decrease in the prices of the oil and gas products. Net profit reached RMB161 billion, up 8.3% YoY, hitting a record high. A final dividend of RMB 0.23 per share was declared. Together with the interim dividend of RMB 0.21 per share, the annual dividend payout rate reached 50% with a yield of 6.6%.

Crude oil production remained stable with increases, while natural gas production continued to grow rapidly, leading to a sustained increase in the proportion of natural gas in overall oil and gas production. In 2023, the Group’s crude oil output amounted to 937 million barrels, representing an YoY increase of 3.4%. The marketable natural gas output reached 4.9 trillion cubic feet, representing an YoY increase of 5.5%. The oil and natural gas equivalent output amounted to 1.759 billion barrels, up 4.4% YoY. Sales volume continued to improve with the volume of gasoline, kerosene and diesel up 10% YoY to a total of 165.798 million tons. While the Group sold 273.548 billion cubic metres of natural gas, up 5.1% YoY. It is recommended to buy at HK$7.30, target at HK$8.50, and stop loss at HK$7.00.

CNOOC(883.HK)’s revenues in FY23 decreased by 1.3% to RMB416 billion, mainly due to the decline of international oil price but partly offset by the increase of oil and gas sales volume. Net profit decreased by 12.6% YoY to RMB123 billion. A final dividend of RMB 0.66 per share was declared. Together with the interim dividend of RMB 0.59 per share, the annual dividend payout rate reached 48% with a yield of 6.7%.

In 2023, the Company achieved crude and liquids sales volume of 514.5 million barrels, an increase of 7.5% YoY with average realised oil price of US$77.96 per barrel, representing a YoY decrease of 19.3%, basically in line with international oil prices. CNOOC increased its exploration and development efforts in offshore China, and the production and sales volume continued to increase, with natural gas sales volume reaching 807.4 bcf, representing a YoY increase of 11.2%. The average realized natural gas price was US$7.98/mcf, representing a YoY decrease of about 7.0%, mainly because the impacts of the Russia-Ukraine conflicts on international natural gas prices have gradually diminished, leading to a relief of supply tensions and a subsequent return of gas prices to a reasonable level. It is recommended to buy at HK$19.10, target at HK$22.25, and stop loss at HK$18.30.

HSI:

Source:Bloomberg

Key events for the week:

- CTG Duty Free (1880.HK) net profit in Q1 amounted to RMB2.3 billion, a YoY increase of 0.3%

- Tianqi Lithium (9696.HK) expected a net loss of RMB 3.6 billion to RMB 4.3 billion in Q1, turning a profit into a loss.

- China Mobile (941.HK) net profit in Q1 increased 5.5% YoY to RMB29.6 billion

- Ping An Insurance(2318.HK) net profit in Q1 stood at RMB36 billion, down 4.3% YoY

| Key events for next week: | |

|---|---|

|

04/30 |

PMI |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

3.8% |

|

Real estate |

9.2% |

|

Industrial |

3.0% |

|

IT industry |

15.0% |

|

Financial |

6.7% |

|

Energy |

1.2% |

|

Raw material |

1.2% |

|

Medical and health care |

11.2% |

|

Telecommunications |

2.7% |

|

Consumer discretionary |

6.0% |

|

Consumer staples |

6.9% |

Source:Bloomberg

Stock pick: PetroChina(857.HK)

Source:Bloomberg

Stock pick: CNOOC(883.HK)

Source:Bloomberg

Analyst: CHAN Ka Kin (CE Number BHS185)

Disclosure of Interest

Neither the analyst(s) preparing this report nor his associate has any financial interest in; or serves as an officer of the listed corporation covered in this report. The remuneration of the analyst(s) is not directly or indirectly related in any way to the particular opinions or views expressed in this report.