The National Bureau of Statistics announced that the profit of industrial enterprises (above designated size) dropped 22% YoY to CNY887.2bn. Although one cannot be too optimistic on China’s economic outlook, the investment market is less affected by the banking incidents in Europe and America. Meanwhile the amount of northbound flows has increased recently. The short-term performance of A-Shares should be relatively stable. Alibaba (9988 HK) unveiled a corporate restructuring plan, under which six major business groups with their own CEO and board of directors will be establish, paving way for potential independent fund-raising and listings, market expects the move to unlock value. As interest rates in US is likely to peak in 1H23, and there are signs of relaxation of regulations for the technology industry in China, technology stocks are expected to outperform the market.

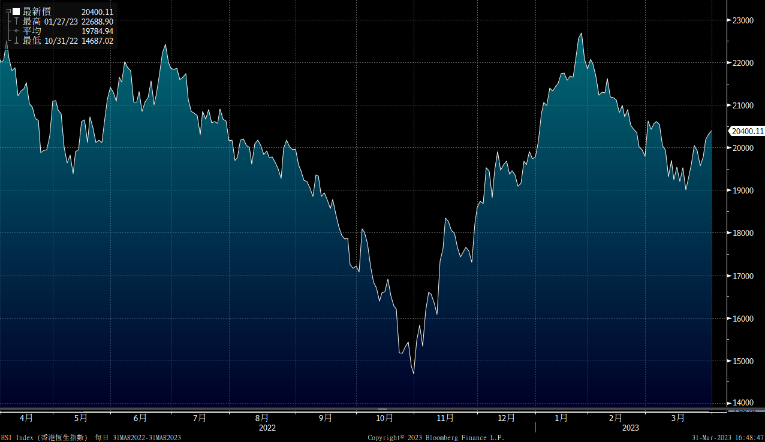

Following the trouble in the US banking industry, the market is also concerned about the European banking industry. Although Deutsche Bank’s CDS touched the highest level since 2020, its fundamentals have improved significantly with profits exceeding 5 bn euros in 2022, reaching a new high since 2007. We believe that the recent correction in the stock prices of financial stocks is mainly due to the lack of confidence. However, the risk of having a financial crisis is not high, the investment market should not be too pessimistic. From the perspective of fund flows, according to EPFR, in March, nearly US$290 bn flowed into the currency market funds, the largest since Covid in 2020. This reflects the fund flow into defensive investment products which may limit the stock market performance. For Hang Seng Index, it regained its 20,000 mark, while the HSI (Volatility Index) of the Hang Seng Index dropped to ~26, reflecting market’s risk aversion has lowered. Technically, Hang Seng index is above 10-days, 20-days and 250-days SMA, however it saw resistance at 50-days SMA (~20,600 level). We expect Hang Seng index to trade between 19,500 -20,600 points.

Supported by the restructuring plan of Alibaba (9988.hk), the technology sector outperformed the market, and we expect the momentum to remain strong in the near term. In addition, as “5/1” holiday is approaching, the retail sector is worth paying attention to.

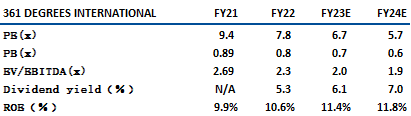

361 DEGREES (1361) is mainly engaged in the manufacturing and sale of 361° branded sports products, including shoes, clothing, and accessories in China. In 2022, 361 Degrees achieved revenue of CNY 6961 mn (+17% YoY) and a net profit of CNY 747mn (+24% YoY). For the revenue breakdown by products, revenue from footwear, which accounted for 41% of the total revenue was CNY 2.854 bn, up 12.7% YoY, revenue from apparel, which accounted for 35% of the total revenue, increased by 14% YoY to CNY2.45 bn. Revenue from kid’s sportswear, which accounted for 20% of total revenue increased by 30.3% YoY to CNY1.44 bn. As of the end of 2022, the company had a total of 5,480 361-degree branded stores, an increase of 210 compared to 2021.

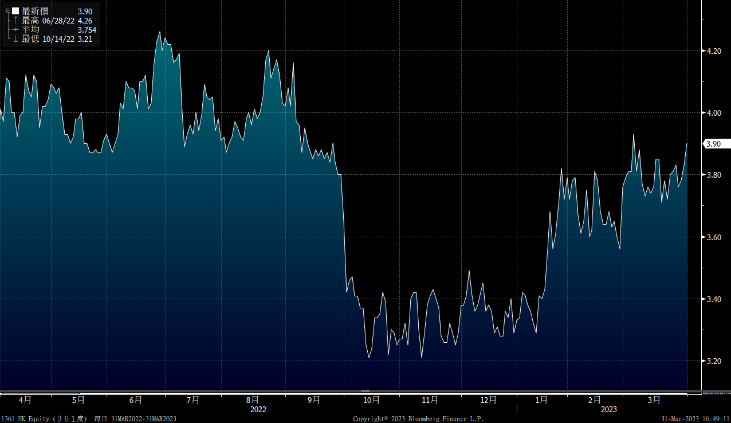

The GPM in 2022 was 40.5%, higher than the 5 years average of 40.1%. Mgmt expects the gross margin to stay between 40-42% in 2023. Due to post covid recovery going well, the adult sportswear growth has achieved 10%+ growth YTD, kid sportswear achieved 20%+ growth YTD and e-commerce growth has also achieved 30%+ growth YTD. Kid’s sportswear growth momentum continues, mgmt plans to open more kid’s sportswear stores in tier 1-2 cities in 2023, and we expect the strategy to accelerate the segment growth. As the 361 DEGREES’ s results outperformed peers and it is being included in stock connect in Mar 23. It is recommended to buy at HK$3.8, target at HK$4.3, stop loss at HK$3.6, Risk. Slower-than-expected sportswear growth.

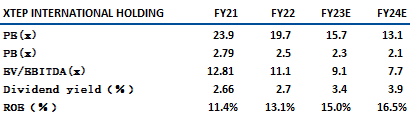

Xtep (1368) is principally engaged in the design, development, manufacturing and marketing of sportswear, including footwear, apparel and accessory products, sold mainly under the self-owned Xtep brand and four internationally acclaimed brands, namely K-Swiss, Palladium, Saucony and Merrell. In 2022, Xtep achieved revenue of CNY 12,930mn (+29% YoY) in which revenue from Mass market (accounting for ~86.1% of total revenue) was +25.9% YoY to CNY 11.128bn. Net profit was +1.5% YoY to CNY922mn, inline with consensus. As of end of 2022, Xtep has an extensive global distribution network and more than 8,000 stores.

Mgmt gave double digit growth guidance for core brand in 2023. As for the inventory, Xtep’s continues to decrease, the inventory turnover day decreased 16 days to 90 days, compared with June 30. Per mgmt., retail inventory level is improving from 5.5 months at the end of 2022 to approx. 5 months in Mar 23. Mgmt said that they aim to decrease inventory to less than 4 months this year. Benefiting from the continuous decrease in inventory, we expect the company to benefit from better cash flow and profit performance. We are optimistic about the continuity of the China Chic trend in the sportswear sector. We think Xtep has its unique edge in low-tier cities and is positive for developing new brands. It is recommended to buy at HK$9.7, target at HK$11.0, stop loss at HK$9.2. Risk. Consumption in China remaining weak.

HSI:

Source:Bloomberg

Key events for the week:

2M23, auto industry revenue was CNY1.28 tn,-6% YoY |

Alibaba(9988.HK) to split into 6 units and explore IPOs |

CHINA RES LAND (1109.HK): FY22 net profit was CNY28.092bn, -13.3% YoY |

Mengniu (02319.HK): FY22 net profit was CNY5.3bn, +5.5% YoY |

China Life (2628.HK): FY22 net profit was CNY32.082 bn -36.8% YoY |

Bank of China (03988.HK): FY22 net profit +5% YoY to CNY227.44 bn |

China Construction Bank (00939.HK): FY22 net profit +7.1% YoY to CNY323.8 bn |

ICBC (01398.HK): ): FY22 net profit +2% YoY to CNY345.67bn |

Agricultural Bank of China (01288.HK): FY22 net profit +7.4% YoY to CNY259.14bn |

Country Garden (02007.HK): FY22 net loss CNY6.052bn |

| Key events for next week: | |

|---|---|

|

04/03 |

HSBC China PMI |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

0.7% |

|

Real estate |

-0.2% |

|

Industrial |

-0.2% |

|

IT industry |

4.9% |

|

Financial |

0.7% |

|

Energy |

3.5% |

|

Raw material |

0.0% |

|

Medical and health care |

-3.2% |

|

Telecommunications |

1.2% |

|

Consumer discretionary |

1.9% |

|

Consumer staples |

-0.7% |

Source:Bloomberg

Stock pick: 361 DEGREES (1361 HK)

Stock pick: Xtep (1368 HK)

Source:Bloomberg

權益披露

研究部分析員及其關連人士沒有持有報告內所推介證券的任何及相關權益;及並無於報告內所推介證券的上市法團擔任高級人員。分析員(等)之報酬不會直接或間接與本報告發表的特定意見或觀點有任何關聯。

滙業證券有限公司與本報告所推介證券的上市法團沒有任何投資銀行業務關係,也沒有任何持有該(等)上市法團市值 1% 或以上的財務權益。此外,滙業證券有限公司的任何僱員概無擔任上市法團的高級人員。

免責聲明

滙業證券有限公司 (「滙業證券」,香港證監會CE編號: AAW265) 的研究部提供以上資料。文內內容及資料未經香港證監會或任何監管機構審核,惟滙業證券會按“證券及期貨事務監察委員會持牌人或註冊人操守準則”內第16條有關分析員的操守準則編制以上資料。為此,以上資料(無論為明示或暗示)均不應視作任何建議、邀約、邀請、宣傳、勸誘、推介或任何種類或形式之陳述。滙業證券或其聯營公司對任何因信賴或參考有關內容所導致的直接或間接損失,概不負責。客戶如以任何方式將以上資料分發予他人,滙業證券或其聯營公司對該些未經許可之轉發不會負上任何責任。投資涉及風險。證券價格可升可跌,買賣證券可導致虧損或盈利。

版權所有

本報告受版權保護,據此,未經滙業證券有限公司明確表示同意,本報告不得用於任何其他目的,也不得出售、分發、出版、或以任何方式轉載。

地址:滙業證券有限公司,香港灣仔告士打道72號六國中心5樓