According to the National Bureau of Statistics, the national consumer price index (CPI) in July rose by 0.5% YoY and 0.5% MoM. Excluding food and energy prices, core CPI rose by 0.4% YoY, maintaining a moderate increase. In July, as consumer demand continued to recover, and due to the high temperatures and rainfalls in some areas, the CPI in July turned from a MoM decline to an increase, and the YoY increase also expanded. Food prices rose by 1.2% MoM, compared to -0.6% in June. Among food, the prices of fresh vegetables and eggs increased by 9.3% and 4.4% MoM respectively. The price of pork increased by 2.0% MoM. With strong demand for summer travel, the prices of airline tickets, travel and hotel accommodation increased by 22.1%, 9.4% and 5.8% respectively. The prices of gold jewelry and gasoline also increased by 1.6% and 1.5% respectively.

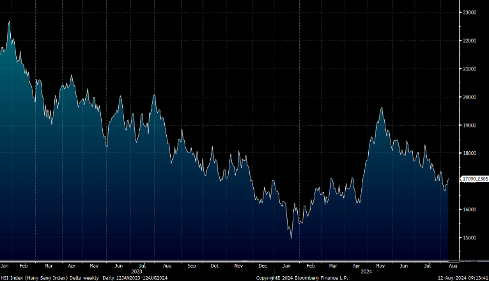

PPI fell by 0.8% YoY in July, same as the previous month. Among that, the price of means of production fell by 0.7%, the decline had narrowed by 0.1 ppts. The price of means of livelihood fell by 1.0%, the decline had expanded by 0.2 ppts. The prices in coal mining and washing and separation industry rose by 0.3%, while non-metallic mineral products dropped by 5.6%. The price of ferrous metal smelting and processing declined by 3.7%, and price of agricultural and sideline products processing industry was down by 2.7%. The price of computer communication and other electronic equipment manufacturers declined by 2.6%. In terms of the Hong Kong stock market, the Hang Seng Index may lack upward momentum in the near term. It is expected to fluctuate between 16,600 – 17,600 points.

Mainland China sees robust travel demand during the summer holidays, which is expected to benefit relative companies.

H World(1179.HK)’s revenue in 1Q24 increased by 17.8% YoY to RMB5.3 billion, surpassing the previous revenue guidance of a 12% to 16% YoY increase. Net income amounted to RMB659 million, down 33% YoY.

In terms of business segment, revenue from leased and owned hotels in 1Q24 stood at RMB3.1 billion, up 7.8% YoY but down 10.3% QoQ. Revenue from manachised and franchised hotels reached RMB2.1 billion, representing a 32.8% YoY increase and a 2.3% QoQ increase. Other revenue includes mainly sales from the provision of IT products and services, Huazhu Mall and other revenue from the Legacy-DH segment, totaling RMB116 million, was up 123% YoY.

As of March 31, 2024, H World operated 9,817 hotels and 955,657 rooms, including 9,684 hotels from Legacy-Huazhu and 133 hotels from DH. As of March 31, 2024, H World had a total of 3,172 to be opened hotels in the pipeline. Looking forward to 2Q24, H World expects its revenue growth to be in the range of 7%- 11%. It is recommended to buy at HK$21.6, target at HK$25.15, and stop loss at HK$20.7.

Tongcheng Travel(780.HK)’s 2Q24 revenue is expected to be in line with the previous guidance, with solid profit. According to Smith Travel Research (STR), China’s hotel occupancy rate fell by a low single-digit YoY over April–June. While the company’s room nights during major holidays still grew faster than the industry average, with domestic room nights rising more than 20% YoY during the Dragon Boat Festival. In terms of Transportation ticketing services segment, in April and May, China’s railway passenger traffic grew 10% and 11% YoY. Domestic airlines experienced growth in passenger traffic by 4% and 8% YoY, while international airlines’ passenger traffic increased by 175% and 132% YoY. The market expect the firm’s train ticket volume growth rate to remain largely similar to the industry and its air ticket volume to grow slightly faster than the industry.

Tongcheng Travel announced on July 30 that it has renewed the strategic cooperation and marketing promotion framework with Tencent. Under the agreement, Tencent will continue to provide Tongcheng with traffic support, advertising and marketing promotion services from Aug 1, 2024 to Jul 31, 2027, and both parties intend to maintain cooperation after contract expiry. This contract renewal shows that Tongcheng secures traffic entry points within WeChat, and its user acquisition and marketing strategies in close partnership with Tencent are likely to remain unchanged. It is recommended to buy at HK$12.95, target at HK$15.05, and stop loss at HK$12.4.

HSI:

Source:Bloomberg

Key events for the week:

- Midea Real Estate (3990.HK) expected interim net profit to drop by up to 66%

- MGM China (2282.HK) interim net profit amounted to HK$2.7 billion, up 2.3 times

- Hua Hong Semiconductor (1347.HK)’s Q2 net profit fell 91.5% YoY to US$6.67 million

- SMIC (981.HK)’s second quarter net profit fell 59.1% YoY to US$165 million

| Key events for next week: | |

|---|---|

|

08/15 |

Retail Sales YoY |

Sector performance:

| 1week performance (%) | |

|---|---|

|

Utilities |

1.9% |

|

Real estate |

4.1% |

|

Industrial |

-1.8% |

|

IT industry |

2.4% |

|

Financial |

-0.5% |

|

Energy |

-1.7% |

|

Raw material |

-1.8% |

|

Medical and health care |

4.7% |

|

Telecommunications |

-3.9% |

|

Consumer discretionary |

0.9% |

|

Consumer staples |

1.9% |

Source:Bloomberg

Stock pick: H World(1179.HK)

Source:Bloomberg

Stock pick: Tongcheng Travel(780.HK)

Source:Bloomberg

Analyst: CHAN Ka Kin (CE Number BHS185)

Disclosure of Interest

Neither the analyst(s) preparing this report nor his associate has any financial interest in; or serves as an officer of the listed corporation covered in this report. The remuneration of the analyst(s) is not directly or indirectly related in any way to the particular opinions or views expressed in this report.