According to the National Bureau of Statistics, the national consumer price index (CPI) in March rose by 0.1% YoY and fell by 1.0% MoM. Excluding food and energy prices, core CPI rose by 0.6% YoY, maintaining a moderate increase. Due to the seasonal decline in consumer demand after the CNY holiday, and the ample market supply, the CPI fell MoM, with lower YoY growth. Food prices fell by 3.2% MoM. The prices of fresh vegetables, pork, eggs, fresh fruits, and aquatic products decreased by 11.0%, 6.7%, 4.5%, 4.2%, and 3.5% MoM, respectively. As March is the travel off-season, air tickets, transportation rental fees and travel prices dropped by 27.4%, 15.9% and 14.2% MoM respectively.

PPI fell by 2.8% YoY in March, about 0.1 ppt more than the previous month. Among that, the price of means of production fell by 3.5%, the decline had expanded by 0.1 ppts. The price of means of livelihood fell by 1.0%, the decline had expanded by 0.1 ppts. The prices in coal mining and washing and selecting industry fell by 15.0%, while non-metallic mineral products dropped by 8.1%. The price of ferrous metal smelting and processing declined by 7.2%, and that of agricultural and sideline products processing industry was down by 4.4%. The price of computer communication and other electronic equipment manufacturers declined by 2.5%. The pace of decline in the above five industries all widened compared to the previous month. In terms of the Hong Kong stock market, the Hang Seng Index is still lacking upward momentum, and it is expected to fluctuate between 16,200-17,200 points.

May Day holiday travel boom has started to heat up in advance, with an increase in flight bookings. The average ticket prices for domestic routes have already surpassed those of the Qingming holiday, signaling continued momentum for the travel sector.

H World (1179.HK) achieved significant growth in 4Q23, reflecting its strong competitive edge and leadership position in the industry. In 4Q23, revenue increased by 50.7% YoY to RMB 5.6 billion, exceeding the previous guidance. In terms of business segments, revenue from leased and owned hotels reached RMB 3.5 billion, a YoY increase of 40.9%. Revenue from managed and franchised hotels stood at RMB 2 billion, marking a 74.1% YoY increase.

The net profit in Q4 amounted to RMB 743 million, compared to a net loss of RMB 124 million in 4Q22, representing a notable turnaround from loss to profit. Looking ahead to 2024, H World expects revenue to grow by 12%-16% YoY Q1, with annual revenue growth between 8%-12%. The group plans to open approximately 1,800 new hotels in 2024 and close around 650 hotels, which indicates that H World will continue to actively expand its scale and optimize its hotel mix to adapt to market changes and customer demands. It is recommended to buy at HK$29.40, target at HK$34.30, and stop loss at HK$28.20.

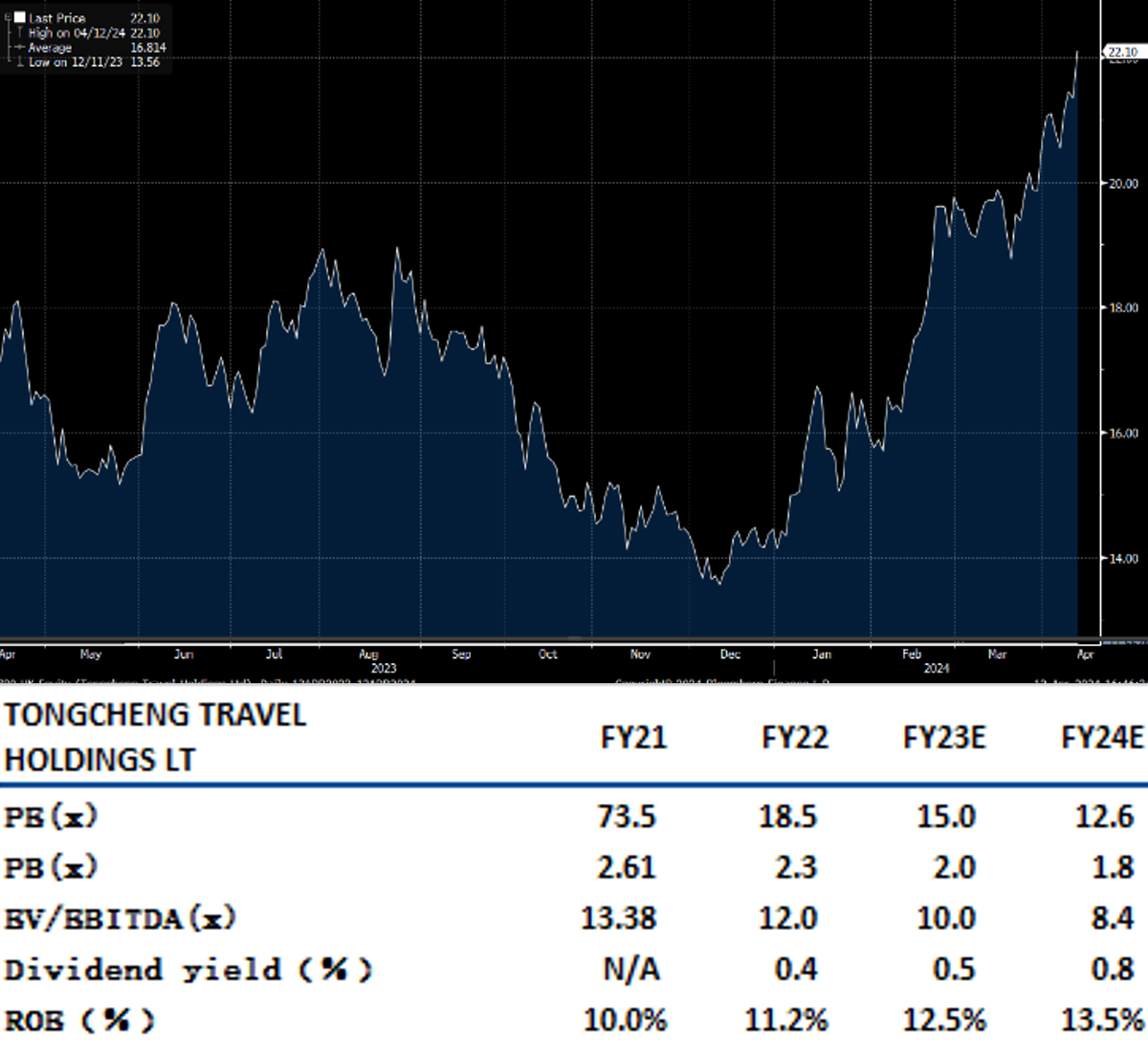

Tongcheng Travel (780.HK)’s revenue in FY23 surge by 80.7% YoY to reach RMB 11.9 billion, primarily attributed to the robust recovery of the travel market and its continuous innovation in products and services and market expansion. The profitability significantly improved. The adjusted EBITDA grew by 117.4% YoY to RMB 3.1 billion, with the adjusted EBITDA margin up from 21.8% in FY22 to 26.3% in FY23. The adjusted net profit increased by 240.3% YoY to RMB 2.2 billion, with the adjusted net profit margin climbing from 9.8% to 18.5%.

The average monthly paying users (MPU) grew by 39.1% YoY from 29.7 million in FY22 to 41.3 million in FY23. Meanwhile, the average annual paying users (APU) rose by 25.2% YoY from 187.5 million to 234.7 million, reflecting the steady expansion in client base and market share. Looking ahead, Tongcheng Travel would continue to expand its business scale and enhance the quality of its products and services by leveraging its market leadership and technological edge, aiming to meet the market demands and drive substantial growth. It is recommended to buy at HK$21.50, target at HK$25.0, and stop loss at HK$20.50.

HSI:

Source: Bloomberg

Key events for the week:

- AEON Credit (900.HK) FY2/24 revenue was HK$1.62 billion, up 31.8% YoY

- CTG Duty Free (1880.HK) Q1 revenue amounted to RMB18.8 billion, down 9.45% YoY

- 361 Degrees (1361.HK) main brand’s offline retail sales recorded high double-digit YoY growth

- Chenming Paper (1812.HK) Q1 net profit ranged from RMB50 million to 70 million, compared with a loss of RMB270 million in the same period last year

| Key events for next week | |

|---|---|

|

04/16 |

Fixed assets estimates YoY、Retail Sales YoY、Industry, value added YoY |

Sector performance:

| 1 week performance (%) | |

|---|---|

|

Utilities |

3.5% |

|

Real estate |

-2.2% |

|

Industrial |

1.9% |

|

IT industry |

0.8% |

|

Financial |

-1.1% |

|

Energy |

1.8% |

|

Raw material |

6.5% |

|

Medical and health care |

0.5% |

|

Telecommunications |

1.5% |

|

Consumer discretionary |

1.5% |

|

Consumer staples |

-1.8% |

Source: Bloomberg

Stock pick: H World (1179.HK)

Source: Bloomberg

Stock pick: Tongcheng Travel (780.HK)

Source: Bloomberg

Analyst: CHAN Ka Kin (CE Number BHS185)

Disclosure of Interest

Neither the analyst(s) preparing this report nor his associate has any financial interest in; or serves as an officer of the listed corporation covered in this report. The remuneration of the analyst(s) is not directly or indirectly related in any way to the particular opinions or views expressed in this report.